5 Time value of money

Compinding future value FV

Discounting present value PV

Interest rate exchange rate between earlier and later money

?FV = PV(1 + r)t

?PV = FV / (1 + r)t

?r = period interest rate, expressed as a decimal

?t = number of periods

?Future value interest factor = (1 + r)t复利终值系数

?1/(1+r) t present value factor 现值系数

For a given interest rate – the longer the time period, the lower the present value

For a given time period – the higher the interest rate, the smaller the present value

?r = (FV / PV)1/t– 1

?t = ln(FV / PV) / ln(1 + r)

6 Discounted Cash Flow Valuation

?Future and Present Values of Multiple Cash Flows

You think you will be able to deposit $4,000 at the end of each of the next three years in a bank account paying 8 percent interest、You currently have $7,000 in the account、How much will you have in three years? In four years?

Today (year 0 CF): 3 N; 8 I/Y; -7,000 PV; CPT FV = 8,817、98 FV = 7000(1、08)3 = 8,817、98 Year 1 CF: 2 N; 8 I/Y; -4000 PV; CPT FV = 4,665、60 FV = 4,000(1、08)2 = 4,665、60

Year 2 CF: 1 N; 8 I/Y; -4000 PV; CPT FV = 4,320 FV = 4,000(1、08) = 4,320

Year 3 CF: value = 4,000

Total value in 3 years = 8817、98 + 4665、60 + 4320 + 4000 = 21,803、58

Value at year 4: 1 N; 8 I/Y; -21803、58 PV; CPT FV = 23,547、87

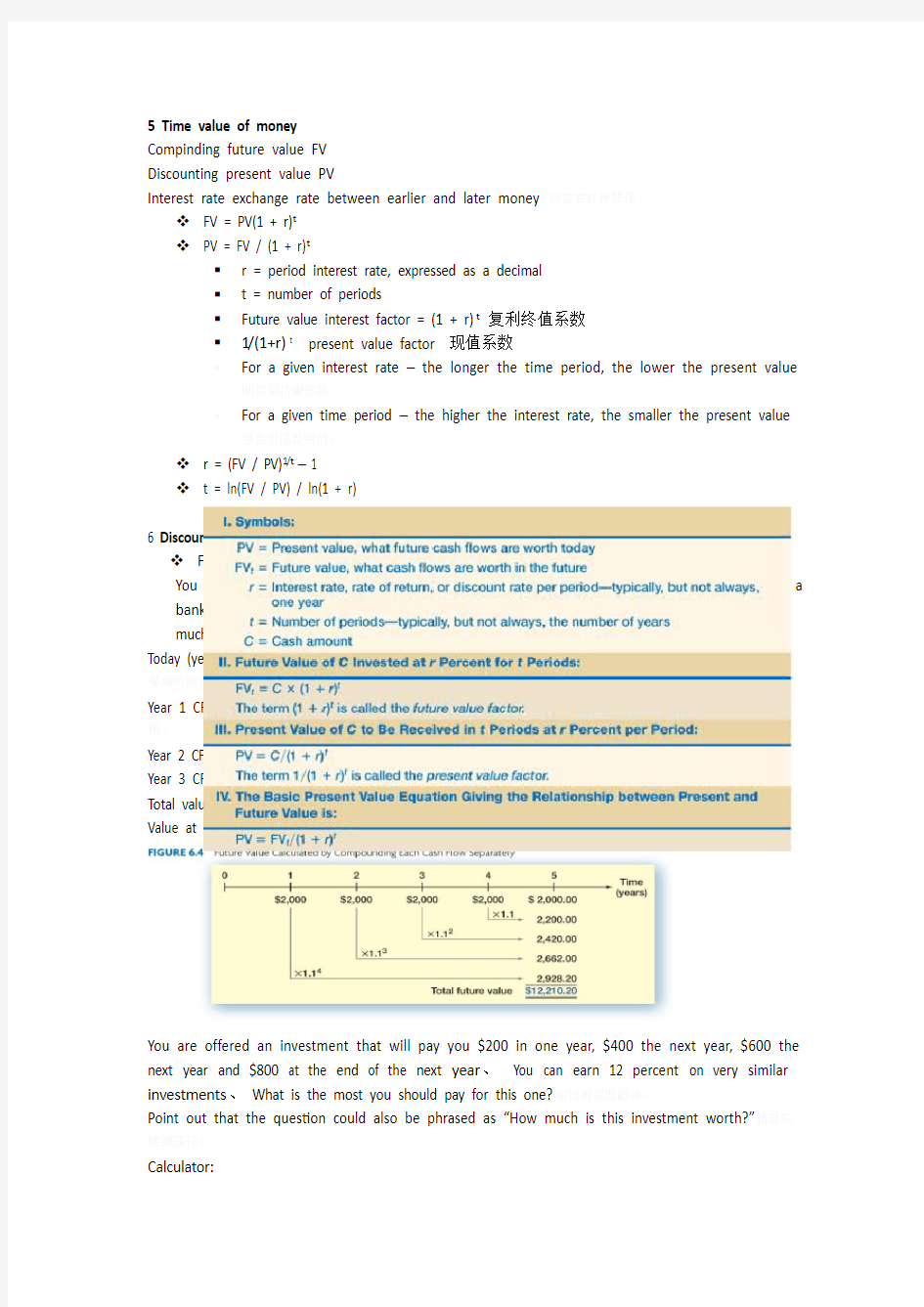

You are offered an investment that will pay you $200 in one year, $400 the next year, $600 the next year and $800 at the end of the next year、You can earn 12 percent on very similar investments、What is the most you should pay for this one?

Point out that the question could also be phrased as “How much is this investment worth?”Calculator:

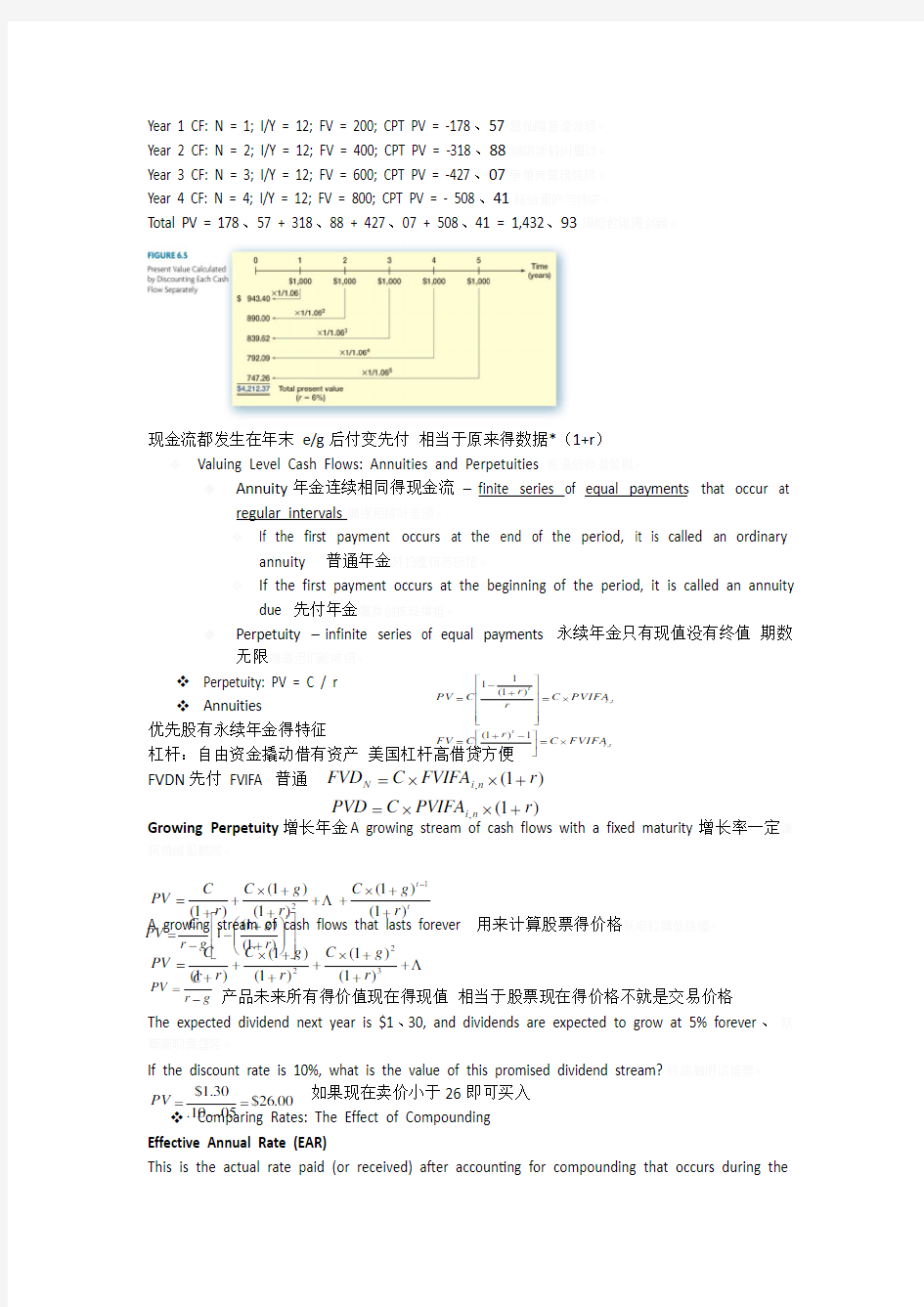

Year 1 CF: N = 1; I/Y = 12; FV = 200; CPT PV = -178、57Year 2 CF: N = 2; I/Y = 12; FV = 400; CPT PV = -318、88Year 3 CF: N = 3; I/Y = 12; FV = 600; CPT PV = -427、07Year 4 CF: N = 4; I/Y = 12; FV = 800; CPT PV = - 508、41Total PV = 178、57 + 318、88 + 427、07 + 508、41 = 1,432、93

现金流都发生在年末 e/g 后付变先付 相当于原来得数据*(1+r )

Valuing Level Cash Flows: Annuities and Perpetuities Annuity 年金连续相同得现金流 – finite series of equal payments that occur at

regular intervals 曠緩颟鎵叶洼颁。If the first payment occurs at the end of the period, it is called an ordinary

annuity 普通年金If the first payment occurs at the beginning of the period, it is called an annuity

due 先付年金Perpetuity – infinite series of equal payments 永续年金只有现值没有终值 期数

无限? Perpetuity: PV = C / r ? Annuities 优先股有永续年金得特征

杠杆:自由资金撬动借有资产 美国杠杆高借贷方便

FVDN 先付 FVIFA 普通 Growing Perpetuity 增长年金A growing stream of cash flows with a fixed maturity 增长率一定

A growing stream of cash flows that lasts forever 用来计算股票得价格 产品未来所有得价值现在得现值 相当于股票现在得价格不就是交易价格

The expected dividend next year is $1、30, and dividends are expected to grow at 5% forever 、 If the discount rate is 10%, what is the value of this promised dividend stream?如果现在卖价小于26即可买入

? Comparing Rates: The Effect of Compounding

Effective Annual Rate (EAR)

This is the actual rate paid (or received) after accounting for compounding that occurs during the t r t t

r t

FVIFA C r r C FV PVIFA C r r C PV ,,1)1()1(11?=??

????-+=?=????????????+-=)

1(,r FVIFA C FVD n i N +??=)

1(,r PVIFA C PVD n i +??=t t r g C r g C r C PV )1()1()1()1()1(12++?++++?++=

-Λ?

??????????? ??++--=t r g g r C PV )1()1(1Λ+++?+++?++=3

2

2)1()1()1()1()1(r g C r g C r C PV g r C PV -=00.26$05.10.30.1$=-=PV

year。If you want to compare two alternative investments with different compounding periods,

比较不同期间得rate不能直接比较

Annual Percentage Rate(APR

?

By definition APR = period rate times the number of periods per year

Consequently, to get the period rate we rearrange the APR equation:

?Period rate = APR / number of periods per year

You should NEVER divide the effective rate by the number of periods per year – it will NOT give you the period rate

Continuous Compounding EAR = e q– 1

Example: What is the effective annual rate of 7% compounded continuously?

EAR = e、07– 1 = 、0725 or 7、25%

Pure Discount Loans

The principal amount is repaid at some future date, without any periodic interest payments、纯折现贷款中间不付息例如Treasury bills

Interest-Only Loan 每年支付利息到期一次性还本金加最后一次利息

Pay interest each period and repay the entire principal at some point in the future

This cash flow stream is similar to the cash flows on corporate bonds、鰥堯頭缍誤网奮。

?Loan Types and Loan Amortization 每年偿还利息加一部分本金

?Make single, fixed payment every period

?5,000=C*{[1-(1/1、095)]/0、09}

?C=1285、45

7 Interest Rates and Bond Valuation

现金流折现得三个重要信息现金流折现率期限评估资产价值对资产未来产生得现金流进行估计把所有现金流折现加总得到零时刻得价值(价值大于价格则买进)?Bonds and Bond Valuation

Par value (face value) – the principal 本金

Coupon rate – fixed when the bond issued票面利率发行方许诺支付

1

m

rate

Quoted

1

EAR

m

-

??

?

??

?

+

=

??

?

??

?+

=1-

EAR)

(1

m

APR m1

Coupon payment – par value * coupon rate

Maturity date 到期日票面利息

Yield or Yield to maturity – interest rate required in market on a bond 持有到期收益率

Bond Value = PV of coupons + PV of par

Bond Value = PV of annuity + PV of lump sum 本金现值

,bond prices decrease

C:cash flow 左侧年金复利系数右侧本金折现

由于市场利率就是变化得,发行时候算得就是发行当时得市场利率,而后可能变化因此到期日要瞧到期日利率YTM

If YTM > coupon rate, then par value > bond price The discount provides yield above coupon rate

Price below par value, called a discount bond

平价债券par bond 折现出来得价值就就是面值

?Coupon rate小于market折价债券discount bond

Consider a bond with a coupon rate of 10% and annual coupons、The par value is $1,000, and the bond has 5 years to maturity、The market interest rate is 11%、What is the value of the bond?

B = PV of annuity + PV of lump sum

B = 100[1 – 1/(1、11)5] / 、11 + 1,000 / (1、11)5

B = 369、59 + 593、45 = 963、04

Coupon rate大于market溢价债券premium bond

Coupon and Yield

?If YTM = coupon rate, then par value = bond price

?If YTM < coupon rate, then par value < bond price

?Why? Higher coupon rate causes value above par

?Price above par value, called a premium bond

Interest Rate Risk(IRR)the risk that arises for bond owners from fluctuating interest rate

利率风险市场得利率变化会导致债券价格得变化

All other things being equal, the long the time to maturity, the greater the interest rate risk All other things being equal, the lower the coupon rate, the greater the interest rate risk

两个除了期限以外全部相同得债券债券条款:

?Debt :hort long term borrowing 债务融资

?Not an ownership interest

?Creditors do not have voting rights

Interest is considered a cost of doing business and is tax deductible

Creditors have legal recourse if interest or principal payments are missed

Excess debt can lead to financial distress and bankruptcy

?Equity :onership interest 权益融资

?Ownership interest

Common stockholders vote for the board of directors and other issues

Dividends are not considered a cost of doing business and are not tax deductible

Dividends are not a liability of the firm, and stockholders have no legal recourse

if dividends are not paid

An all equity firm can not go bankrupt merely due to debt since it has no debt

利息抵税债权人不参与管理借钱方式有两种银行贷款与发股票

The Bond Indenture 债券契约

Contract between the company and the bondholders that includes

?The basic terms of the bonds 基本条款

?The total amount of bonds issued 发行总额

A description of property used as security, if applicable担保说明有形资产做

抵押品

?Sinking fund provisions偿债基金条款

?Call provisions 赎回条款

?Details of protective covenants 保护性条款

?价格受条款影响有抵押价格高、偿债基金高、没有赎回条款高、有保护条款高Bond Classifications

?Registered记名债券Bearer Forms 无记名债券国库券认券不认人

?Security担保性质

Collateral – secured by financial securities质押债券质押物通常为公司普通股

Mortgage – secured by real property, normally land or buildings 抵押债券通

常为不动产

?Debentures – unsecured 信用债券无担保债券以企业信用发行

Notes – unsecured debt with original maturity less than 10 years ?Seniority 优先权比次级债券更优先获得补偿

?Bond Ratings

High Grade

Moody’s Aaa and S&P AAA – capacity to pay is extremely strong 标准普尔

Moody’s Aa and S&P AA – capacity to pay is very strong

Medium Grade 还款能力强但受环境变化

Moody’s A and S&P A – capacity to pay is strong, but more susceptible to changes in

circumstances

Moody’s Baa and S&P BBB –capacity to pay is adequate, adverse conditions will

have more impact on the firm’s ability to pay

Bond ratings are concerned only with the possibility of default

Low Grade

Moody’s Ba and B

S&P BB and B

Considered possible that the capacity to pay will degenerate、还款能力具有投机

性

Very Low Grade垃圾债券

Moody’s C (and below) and S&P C (and below)

income bonds with no interest being paid, or

?in default with principal and interest in arrears

?Some Different Types of Bonds

Government Bonds

Treasury Securities

Federal government debt 国债

T-bills – pure discount bonds with original maturity of one year or less

T-notes – coupon debt with original maturity between one and ten years

T-bonds – coupon debt with original maturity greater than ten years Municipal Securities

Debt of state and local governments

Varying degrees of default risk, rated similar to corporate debt

Interest received is tax-exempt at the federal level 部分地方政府债可免部分税

?Bond Markets

Zero Coupon Bonds

Make no periodic interest payments (coupon rate = 0%)完全无票息得债券

The entire yield-to-maturity comes from the difference between the purchase price and the par

value

Cannot sell for more than par value 发行价不能高于面值

Sometimes called zeroes, deep discount bonds, or original issue discount bonds (OIDs)

Treasury Bills and principal-only Treasury strips are good examples of zeroes面值发行折扣债券

Floating-Rate Bonds

Coupon rate floats depending on some index value

Examples – adjustable rate mortgages and inflation-linked Treasuries

There is less price risk with floating rate bonds

The coupon floats, so it is less likely to differ substantially from the yield-to-maturity

Coupons may have a “collar” –the rate cannot go above a specified “ceiling” or below a specified “floor

Other Bond Types

Cat bonds大灾债券

Income bonds 收益债券票息随公司收益波动

Convertible bonds 可转换债券可转换为股票

Put bonds(call)债券持有者有权要求发行方按照一定价格回购以保护持有者利益

Bond Markets

Trading volume is much larger than volume in stocks

Primarily over-the-counter transactions with dealers connected electronically

Extremely large number of bond issues, but generally low daily volume in single issues

Makes getting up-to-date prices difficult, particularly on small company or municipal issues

?Treasury Quotations Highlighted quote in Figure 7、4

Nov 2021 8 136:29 136:30 5 4、36

到期日票面利率/买卖价差bidask 相比昨天变化分母为32

What is the coupon rate on the bond?

When does the bond mature?

What is the bid price? What does this mean?

What is the ask price? What does this mean?

How much did the price change from the previous day?

What is the yield based on the ask price?

Clean price: quoted price净价/报价

Dirty price: price actually paid = quoted price plus accrued interest 含息价

Example: Consider a T-bond with a 4% semiannual yield and a clean price of $1,282、50:

Number of days since last coupon = 61

Number of days in the coupon period = 184

Accrued interest = (61/184)(、04*1000) = $13、26

Dirty price = $1,282、50 + $13、26 = $1,295、76

So, you would actually pay $ 1,295、76 for the bond

8 Stock Valuation

? Common Stock Valuation

If you buy a share of stock, you can receive cash in two ways The company pays dividends

You sell your shares, either to another investor in the market or back to the company As with bonds, the price of the stock is the present value of these expected cash flows 估计股利Estimating Dividends: Special Cases

Constant dividend 高速增长不长久 达到稳定

The firm will pay a constant dividend forever

This is like preferred stock

The price is computed using the perpetuity formula

Constant dividend growth

The firm will increase the dividend by a constant percent every period The price is computed using the growing perpetuity model Supernormal growth

Dividend growth is not consistent initially, but settles down to constant growth eventually The price is computed using a multistage model

Zero Growth

If dividends are expected at regular intervals forever, then this is a perpetuity and the present value of expected future dividends can be found using the perpetuity formula P 0 = D / R 必要报酬率

Dividend Growth Model

Dividends are expected to grow at a constant percent per period 、P0 = D1 /(1+R) + D2 /(1+R)2 + D3 /(1+R)3 + …

P0 = D0(1+g)/(1+R) + D0(1+g)2/(1+R)2 + D0(1+g)3/(1+R)3 + … 股利增长模型 注意: just paid a dividend 与is expected to pay 可以得到得就是D0预期得就是1Nonconstant Growth Problem Statement 不稳定增长

Suppose a firm is expected to increase dividends by 20% in one year and by 15% in two years 、 After that, dividends will increase at a rate of 5% per year indefinitely 、 If the last dividend was $1 and the required return is 20%, what is the price of the stock?Remember that we have to find the PV of all expected future dividends 、 Compute the dividends until growth levels off

D 1 = 1(1、2) = $1、20

D 2 = 1、20(1、15) = $1、38

D 3 = 1、38(1、05) = $1、449

Find the expected future price

P 2 = D 3 / (R – g) = 1、449 / (、2 - 、05) = 9、66

Find the present value of the expected future cash flows g

-R D g -R g)1(D P 1

00=+=

P0 = 1、20 / (1、2) + (1、38 + 9、66) / (1、2)2 = 8、67 股利增长模型求R

对投资者必要报酬率

对企业获取资金得成本

普通股得feature

Voting Rights 股东投票权

Proxy voting代理投票

Classes of stock 我国无股票分级一股一票

Other Rights

Share proportionally in declared dividends

Share proportionally in remaining assets during liquidation

Preemptive right – first shot at new stock issue to maintain proportional ownership if desired 优先认股保持比例防止稀释

9 Net Present Value and Other Investment Criteria

when evaluating capital budgeting decision rules:4个标准

?Does xx account for the time value of money?

?Does xx account for the risk of the cash flows?

Does xxprovide an indication about the increase in value?

Should we consider xx for our primary decision rule?

Net Present Value:

difference between the market value of a project and its cost

How much value is created from undertaking an investment?

? 1 estimate the expected future cash flows、

2 estimate the required return for projects of this risk level、

3 find the present value of the cash flows and subtract the initial investment、

Decision rule: If the NPV is positive, accept the project NPV正就接受the project is expected to add value to the firm and will therefore increase the wealth of the owners、

Since our goal is to increase owner wealth, NPV is a direct measure of how well this project will meet our goal、

NPV=-30,000+6,000*[1-(1/1、15)8)]/0、15+(2000/1、158) =-2,422

Payback Period

How long does it take to get the initial cost back in a nominal sense?

Computation

g

P

D

g

P

g)

1(

D

R

g-

R

D

g-

R

g)

1(

D

P

1

1

+

=

+

+

=

=

+

=

Estimate the cash flows

Subtract the future cash flows from the initial cost until the initial investment has been recovered

decision Rule Accept if the payback period is less than some preset limit

Year 1: 165,000 – 63,120 = 101,880 still to recover

?Year 2: 101,880 – 70,800 = 31,080 still to recover

Year 3: 31,080 – 91,080 = -60,000 project pays back in year 3

Advantages and Disadvantages of Payback

?Easy to understand

?Adjusts for uncertainty of later cash flows

?Biased toward liquidity

?Risk screening device

Disadvantage

?Ignores the time value of money

?Requires an arbitrary cutoff point

?Ignores cash flows beyond the cutoff date

Biased against long-term projects, such as research and development, and new projects

NPV(short)=-250+100/1、15+200/1、

152=-11、81

NPV(long)=-250+100*[1-(1/1、154)]/0、

15=35、50

?The Discounted Payback

Compute the present value of each cash

flow and then determine how long it takes

to pay back on a discounted basis箫誰缨臥

维璎镇。

Compare to a specified required period

Decision Rule - Accept the project if it pays back on a discounted basis within the specified time

?Year 1: 165,000 – 63,120/1、121 = 108,643

?Year 2: 108,643 – 70,800/1、122 = 52,202

Year 3: 52,202 – 91,080/1、123 = -12,627 project pays back in year 3

评价The answer to the first two questions is yes、

The answer to the third question is no because of the arbitrary cut-off date、

Since the rule does not indicate whether or not we are creating value for the firm, it should not be the primary decision rule、

Advantages and Disadvantages of Discounted Payback

?The Average Accounting Return AAR多种定义

Average net income / average book value

Note that the average book value depends on how the asset is depreciated、

Need to have a target cutoff rate

Decision Rule: Accept the project if the AAR is greater than a preset rate沪辭违埘卺谛诱。Assume we require an AAR = 25%

Average Net Income:(13,620 + 3,300 + 29,100) / 3 = 15,340

AAR = 15,340 / 72,000 = 、213 = 21、3% reject

?Advantages and Disadvantages of AAR

Ad Easy to calculate/Needed information will usually be available

Disadvantages

Not a true rate of return; time value of money is ignored

?Uses an arbitrary benchmark cutoff rate

Based on accounting NI and book values, not CF and MV

?The Internal Rate of Return (IRR) NPV最好得替代

It is often used in practice and is intuitively appealing

It is based entirely on the estimated CF and is independent of interest rates found elsewhere

Definition: IRR is the return that makes the NPV = 0

Decision Rule: Accept if the IRR is greater than the required return

The IRR rule accounts for time value because it is finding the rate of return that equates all of the cash flows on a time value basis、

The IRR rule accounts for the risk of the cash flows because you compare it to the required return, which is determined by the risk of the project、

The IRR rule provides an indication of value because we will always increase value if we can earn a return greater than our required return、

We should consider the IRR rule as our primary decision criteria, but as we will see, it has some problems that the NPV does not have、That is why we end up choosing the NPV as our ultimate decision rule、

Advantages

Knowing a return is intuitively appealing

It is a simple way to communicate the value of a project to someone who doesn’t know all the

estimation details

If the IRR is high enough, you may not need to estimate a required return, which is often a difficult task

NPV vs、IRR

?多数情况结果一致

?Exceptions

Nonconventional cash flows – cash flow signs change more than once

When the cash flows change sign more than once, there is more than one IRR

When you solve for IRR you are solving for the root of an equation, and when you cross the x-axis more than once, there will be more than one return that solves the equation

If you have more than one IRR, which one do you use to make your decision?

The NPV is positive at a required return of 15%, so you should Accept

If you use the financial calculator, you would get an IRR of 10、11% which would tell you to Reject

You need to recognize that there are non-conventional cash flows and look at the NPV profile

?Mutually exclusive projects

Initial investments are substantially different (issue of scale)

?Timing of cash flows is substantially different

Mutually exclusive projects

If you choos e one, you can’t choose the other

Example: You can choose to attend graduate school at either Harvard or Stanford,

but not both

Intuitively, you would use the following decision rules:

NPV – choose the project with the higher NPV

IRR – choose the project with the higher IRR

有矛盾NPV directly measures the increase in value to the firm就用NPV

Modified IRR

Calculate the net present value of all cash outflows using the borrowing rate、

Calculate the net future value of all cash inflows using the investing rate、

Find the rate of return that equates these values、

Benefits: single answer and specific rates for borrowing and reinvestment

?The Profitability Index

Measures the benefit per unit cost, based on the time value of money

A profitability index of 1、1 implies that for every $1 of investment, we create an additional $0、

10 in value

Advantages

Closely related to NPV, generally leading to identical decisions

Easy to understand and communicate

May be useful when available investment funds are limited

This measure can be very useful in situations in which we have limited capital

Disadvantages

May lead to incorrect decisions in comparisons of mutually exclusive investments

The Practice of Capital Budgeting 做决定时候要考虑好多investment criteria NPV IRR 最常用Payback is a commonly used secondary investment criteria

Summary – DCF Criteria

?Net present value

?Difference between market value and cost

?Take the project if the NPV is positive

?Has no serious problems

?Preferred decision criterion

?Internal rate of return

?Discount rate that makes NPV = 0

Take the project if the IRR is greater than the required return

?Same decision as NPV with conventional cash flows

IRR is unreliable with nonconventional cash flows or mutually exclusive projects

?Profitability Index

?Benefit-cost ratio

?Take investment if PI > 1

?Cannot be used to rank mutually exclusive projects

May be used to rank projects in the presence of capital rationing ?Payback period

Length of time until initial investment is recovered

Take the project if it pays back within some specified period

Doesn’t account for time value of money, and there is an arbitrary cutoff period

?Discounted payback period

Length of time until initial investment is recovered on a discounted basis

Take the project if it pays back in some specified period

?There is an arbitrary cutoff period

?Average Accounting Return

Measure of accounting profit relative to book value

?Similar to return on assets measure

Take the investment if the AAR exceeds some specified return level

?Serious problems and should not be used

北大经院金融考研罗斯《公司理财》终 极笔记 第六篇期权与公司理财 第二十二章期权与公司理财 22.1期权 期权:是一种赋予持有人在某给定日期或该日期之前的任何时间以固定价格购进或售出一种资产之权利的合约。关于期权有一个专门的词汇表,以下是一些重要定义: 1、执行期权。 2、敲定价格或执行价格。 3、到期日。 4、美式期权和欧式期权。 22.2看涨期权 看涨期权:赋予持有人在一个特定时期以某一固定价格购进一种资产的权利。 对资产的种类并无限制,但在交易所交易的最常见期权是股票和债券的期权。 看涨期权-看涨期权在到期日的价值 普通股股票的看涨期权合约在到期日的价值是多少呢? -答案取决于标的股票在到期日的价值。 如果在期权到期之日股价更高的话,则看涨期权更有价值。 如果股价高于行权价,则称看涨期权处于实值状态。 22.3看跌期权 看跌期权:可视为看涨期权的对立面。 正如看涨期权赋予持有人以固定价格购进股票的权利那样,看跌期权赋予持有人以固定的执行价格售出股票的权利。 看跌期权-看跌期权在到期日的价值 由于看跌期权赋予持有人售出股份的权利,所以确定看跌期权价值正好与看涨期权相反。如果期权到期时,股价高于执行价格,看跌期权的持有者就不会行权。看跌期权的所有者会放弃期权,即任由期权过期。 22.4售出期权 假如看涨期权持有人提出要求则售出(或签订)普通股股票看涨期权的投资者将履约售出股份。

若在到期日普通股的价格高于执行价格,持有人将执行看涨期权,而期权出售者必须按执行价格将股份卖给持有人。出售者将损失股票价格与执行价格的差价。 与之相反,若在到期日普通股股票的价格低于执行价格,则看涨期权将不被执行,而出售者的债务为零。 如果股价高于行权价,看涨期权的售卖者就要蒙受损失,而他只有在股价低于行权价时,才能避免亏损。 为什么看涨期权的售卖者愿意接受这种不妙的处境呢? -答案是对他们所承担的风险,期权购买者要向其支付一笔钱,即在期权交易发生日,期权的售卖者将从期权的购买者处得到购买者为此支付的报酬。 现在,让我们研究一下看跌期权的售卖者。 如果看跌期权持有人提出要求,出售普通股票看跌期权的投资者将同意购进普通股股票。如果股票价格跌至低于执行价格,而持有人又将这些股票按照执行价格卖给出售者,出售者在这笔交易上将蒙受损失。 22.5期权报价 22.6期权组合 若股价高于执行价格,则看跌期权毫无价值,且组合的价值等于普通股股票的价值。 若执行价格高于股价,则股价的下降正好被看跌期权的价值增加所抵消。 买看跌期权的同时买标的股票的策略被称为保护性看跌期权。 22.7期权定价-看涨期权的价值

第七章 11.敏感性分析与盈亏平衡点我们正评估一个项目,该项目成本为724000美元,存续期限为8年,残值为0。假设在项目生命期内以直线折旧法计提折旧,最终账面值为0。预计每年的销售量为75000单位,每单位的价格为39美元,每单位的可变成本为23美元,每年固定成本为850000美元。税率为35%,我们对该项目要求的收益率为15%。 a.计算会计盈亏平衡点 b.计算基本情况下的现金流与净现值。净现值对销售数额变动的敏感性如何?根据你的答案,说明当预测销售量减少500单位时会发生什么情况? c.营运现金流(OCF)对可变成本数值变动的敏感性如何?根据你的答案,说明当估计的可变成本降低1美元时会发生什么情况? 答案:a.每年的折旧为:724000/8=90,500 会计利润的盈亏平衡点:(固定成本+折旧)/(销售单价-单位变动成本)= (850,000 + 90,500)/(39 – 23)=58781 b.1)基本情况下的现金流为: [(销售单价-可变成本)*销售量-固定成本](1-税率)+税率*折旧=[(39 –23)(75,000) –850,000](0.65) + 0.35(90,500)= 259,175

净现值=-成本+现值现值=年金现值表(15%,8)*现金流 =-724000+259,175(PVIFA15%,8)=439001.55 2)当销售量为80000时,现金流为: [($39 –23)(80,000) –$850,000](0.65) + 0.35($90,500)= 311,175 净现值为:–$724,000 + $311,175(PVIFA15%,8)= 672,342.27 则:销售额变动,净现值变动为: D净现值/D销售量=(439,001.55-672,342.27)/(75,000-80.000)=46.668 如果销售量减少500单位则净现值下降: 46.668*500=23.334 C.可变成本降低一美元时,营运现金流为: [(39 –24)(75,000) –850,000](0.65) + 0.35(90,500)= 210,425 则营运现金流对可变成本的变化: DOCF/Dvc = ($259,175 – 210,425)/($23 – 24)=-48750 即;如果可变成本降低一美元则营运现金流增加48750 14、题财务盈亏平衡点 LJ 玩具公司刚刚购买了一台250000 美元的机器,以生产玩具车。该机器将在其5 年的使用期限内以直线折旧法计提折旧。每件玩具售价为25 美元。每件玩具的可变成本为6 美元,每年公司的固定成本为360000 美元。公司税率为34%。适当的折现率为12%。

第二章:财务比率的计算 (一)反映偿债能力的指标 1、资产负债率 负债总额 流动负债长期负债 宀亠「亠 - X 100% 一 X 100% (资产一负债+所有者权益) 资产总额 负债所有者权益 2、流动比率= 流动资产 X 100% 流动负债 3、速动比率= 速动资产 流动资产-预付账款-存货-待摊费用 X 100% = X 100% 流动负债 流动负债 4、现金比率= 现金(货币资金)短期有价证券(短期投资) X 100% 流动负债 (二)反映资产周转情况的指标 销售收入-现销收入-销售退回、折让、折扣 (期初应收账款 期末应收账款)2 销货成本 销货成本 平均存货(期初存货~~期末存货)2 习题: 1、某公司20 xx 年末有关财务资料如下:流动比率 =200%、速动比率=100%、现金比率=50%、 流动 负债=1000万元,该公司流动资产只包括货币资金、 短期投资、应收账款和存货四个项目 (其 中短期投资是货币资金的 4倍)。要求:根据上述资料计算货币资金、短期投资、应收账款和存 货四个项目的金 额。 2、某公司20 xx 年末有关财务资料如下:流动比率 =200%、速动比率=100%、现金比率=20%、 资产负债率=50%、长期负债与所有者权益的比率为 25%。要求:根据上述资料填列下面的资 公司理财计算题 1、应收账款周转率 赊销收入净额 平均应收账款余额 2、存货周转率

产负债表简表。 资产负债表(简) 3、某公司年初应收账款56万元、年末应收账款60万元,年初存货86万元、年末存货90万元,本年度销售收入 为680万元(其中现销收入480万元,没有销售退回、折让和折扣),销货成 本 为560万元。要求:根据上述资料计算应收账款周转率和存货周转率。 4、某公司20 xx年度全年销售收入为600万元,其中现销收入为260万元,没有销售退回、折让和折扣,年初应 收账款为30万元,年末应收账款比年初增加了20%,则应收账款周转率应该 是多少? 5、某公司20 xx年度全年销货成本为400万元,年初存货为50万元,年末存货比年初增加了20% , 则存货周转率 应该是多少? 第三章:货币时间价值 1、单利:终值=P(1 n)【公式中i为利率,n为计息期数】 现值P = /(1 n) 2、复利:终值= P = P (1)n【公式中(1)n称为复利终值系数,简写作】

金融硕士考研罗斯《公司理财》重点章节3 第五篇长期融资 第十九章公众股的发行 19.1 公开发行 公开发行有两种方法:普通现金发行和配股发行。 公司第一次公开发行股票被称为是首次公开发行(Initial Public Offering,IPO)或非再次新发行。 再次新发行指先前曾发行过证券的公司再发行新股。 两种方式 1.普通现金发行:出售给所有感兴趣的投资者 2.配股发行:出售给现有股东 19.2另一种发行方式 1.首次公开发行(IPO)或非再次发行 2.再次新发行 发行新证券的集中方式:方法 类型定义公 开 发 行传统议价现金发行报销公司和投资银行之间就发行股票或债券的承销和分配的协议进行谈判承销人事先确定的一部分股票,然后按较高的价格出售。现金发行现金发行承销 公司要求投资银行按双方同意的价格尽可能多的出售新发行股票。但该方法没有保证究竟可以筹集多少资金。特权认购配股直接 发行 公司直接向现有股东发行新股。 附权备用 发行 与配股直接发行一样,这种方法包含一份与现有股东关于特权认购的协议。发行收入由承销商予以保证。费传统的 现金发行上架现金发行有资格的公司可以取得它们在未来两年的期间预计所有要发行股票的许可权,当需要时再出售他们。

公司现金 竞价发行 公司可以通过公开拍卖,而不是协商来选择如何订立承销合同。 私下发行私下直接 发行 将证券直接出售给购买者,后者至少在两年内不得再行出售。 19.3现金发行 投资银行:提供广泛多样服务的金融中介机构。除了帮助证券销售,他们可以促成兼并和其他形式的公司重组,充当客户和机构客户双方面的经纪人,以及用他们自己的账户进行交易。 投资银行提供如下各类服务: ●制定证券发行的价格; ●为新发行证券定价; ●销售新发行证券; ●通过发行证券来获取现金有两种基本的方法:包销和承销。 差价或折价 承销团 绿鞋条款:该条款给予承销团成员按照发行价增购证券的选择权。 19.3.1投资银行——新证券发行的核心★★★★ 19.3.2发行价——确定发行价最困难 19.3.3折价:一种可能的解释 赢家的诅咒 19.4新股发行公告和公司价值 实证研究表明:在普通新股公告日现有股票的市场价值下挫。可能的解释: 1.管理者信息。(被高估) 2.负债能力。(合理的负债-权益比) 3.盈余下降。 19.5新股发行成本 六类成本: 1.差价或承销折价; 2.其他直接费用;(包括申请费、律师费和税金) 3.间接费用;(没有在招股说明书中公布,包括管理者在新股发行上所花的时间) 4.超常收益; 5.折价;

●净营运资本NWC=流动资产-流动负债 净资本性支出=期末固定资产净额-期初资产净额+折旧 息税前利润EBIT=收入-成本-折旧-其他费用+其他利润 边际税率:多装亿美元需要支付的税金 公司的价值V=B+S ●会计的现金流量表:经营活动产生的现金流,筹资活动产生的现金流,投资活动产生的现金流 ●财务现金流量表:CF(A)≡ CF(B) + CF(S) 资产的现金流CF(A)=经营现金流OCF【=EBIT+折旧-税=净利润+折旧=销售收入-成本-所得税=(销售收入-成本)*(1-税率)+折旧*税率】-净资本性支出(固定资产的取得减固定资产的处置)-净营运资金的增加 ==企业流向债权人的现金流量CF(B)(利息加到期本金减长期债务融资=利息加去年长期负债减今年长期负债=利息加赎回债务)+企业流向股东的现金流量CF(S)(股利加股票回购减权益融资) ●会计的现金流量表和财务现金流量表有何不同: 1)概念不一样;2)等式不一样; 3)经营现金流的数额不同;4)经营现金流的计算方法不同。 会计现金流量将利息作为营运现金流量,而财务现金流量将利息作为财务现 金流量。会计现金流量的逻辑是,利息在利润表的营运阶段出现,所以在计算 净利润时利息被当做一项费用扣除了。比较这两种现金流量,财务现金流量更 适合衡量公司业绩。 ●有限责任公司:股东以其出资额为限对公司承担责任,公司以其全部资产对公司的债务承担责任。 股份有限公司:其全部资本分为等额股份,股东以其所持股份为限对公司承担责任,公司以其全部资产对公司的债务承担责任。 ●公司投资包括重置投资和净投资。 重置投资:弥补固定资产损耗的投资,维持原有的生产能力。 净投资:扩大固定资产规模的投资。 代理问题:代理人(管理者)与委托人(股东或债权人)的利益不一致。 代理成本:由管理者与股东之间代理问题而引起的成本 直接的代理成本:管理人员的薪酬和在职消费 间接的代理成本:监督管理者而产生的成本 ●利润最大化的缺陷:(1)没有考虑资金的时间价值;(2)没有考虑风险因素; (3) 没有考虑产出和投入之间的比例关系; (4) 没有考虑权益资本的成本。 ●公司理财研究以下三个方面问题: 公司应该投资于什么样的长期资产项目(资本预算) 公司如何筹集所需的资金(资本结构) 公司应该如何管理短期经营活动产生的现金流(净营运资本)

个人银行工作总结理财 银行理财客户经理个人工作总结 大家好!我是来自##支行的##,非常荣幸能够参加这次理财经理的竞聘,首先,请允许我向大家介绍一下我的基本情况。 我今年28岁,2014年毕业于吉林省经济管理学院会计专业,毕业后进入交行 工作先后在原新春储蓄所、储蓄所作储蓄员工作。2014年通过招聘进入延边移动 公司任客户经理。于今年11月份重新回到交行在春晖支行担任临柜柜员。这些工 作经历增加了我的工作经验同时也提高了各个方面的能力。下面就我所具备的竞争条件和优势做简要的介绍。 一、首先我对银行理财工作非常感兴趣,同时也是一个工作勤勉和善于学习的人,我有信心在银行理财岗位能够更好地展现我的价值,并且为我行创造更多的价值。通过06年底开始的股市牛市以来,客户对个人理财方面开始有很大的需求, 但是又凸现出个人理财知识的匮乏,这就需要有专业人士来进行正确的指导,来实现客户和银行的双赢。在为客户办理理财的同时,树立交行个人理财的品牌,来吸引更多的客户。 二、我曾经在移动公司任客户经理,在此期间,积极做好优质客户的营销工作,培养了自身营销的能力;并且通过这段工作经历,使我具有一定的公关能力和良好 的社会关系。我深信,在自己努 力和多方面的支持下,我能出色了做好这项工作。 三、有在一线网点工作的经历,接触的客户层面较多,能够了解各类客户的需求,根据不同类型的客户,而采用有针对性的营销策略。努力做到客户需要什么,我们就要给他什么。让客户把我们当作自己人来看待。 四、如果这次能够竞聘成功,我将从以下几个方面来加强 1、尽快适应岗位转换。首先是加强理财知识。不能够熟悉个人理财业务知识和我们的各种理财产品,得不到客户的信服,任何的服务和营销将无从谈起。更谈不上客户的开发。其次是营销的技能。在理财经理岗位上不单纯是个客户作理财服务,我们的目的是要将我们的产品销售出去,为我行创造效益。我们每天都会面对许多形形色色的客户,要善于和他们进行广泛的沟通与交流,洞察客户的想法,为其提供满意的服务。通过对学习和对市场行情的准确把握,为客户提供合理建议。这种营销,既立足当前,更着眼于未来。善待客户,就是善待自己;提升客户价值,就是提升自我价值。 2、目前,银行理财主要以单一产品销售为主,什么在市场上卖得火,我们就 一拥而上都卖这个,而忽视了必要的个人投资风险 规避。只注重短期效应,比如在去年的基金销售中,个别行就存在这种情况。针对这种情况,我将着重于组合理财产品和手段,由对客户的深入了解开始,然后

(P∕F r 10% r 1) =0.9091 (P/A f 10% r 3 ) =2。4869 (P∕F f 10% r 5) =0。6209 (P∕A f 10% r 4) =3。1699 (P/F r 10% r 6 ) =0。5645 第一章导论 1. 公司目标:为所有者创造价值公司价值在于其产生现金流能力。 2. 财务管理的目标:最大化现有股票的每股现值。 3?公司理财可以看做对一下几个问题逬行研究: 1. 资本预算:公司应该投资什么样的长期资产. 2. 资本结构:公司如何筹集所需要的资金。 4. 公司制度的优点:有限责任,易于转让所有权,永续经营。缺点:公司税对股东的双重课 第二章会计报表与现金流量 资产二负债+所有者权益(非现金顶目有折旧、逼延税款) EBrr (经营性净利润)=净销售额?产品成本?折旧 EBrrDA = EBrr +折旧及摊销 现金流量总额CF (A)=经营性现金流量?资本性支岀?净运营资本増加额=CF(B) + CRS ) 经营性现金流量OCF =息税前利润+折旧?税 净运营资本=流动资产?流动负债 3?净运营资本管理:如何 理短朗经营活动产生的现金流。 资本性输出= 定资产増加额+折旧

第三章财务报表分析与财努模型 1. (流动性指标) 流动t淳=流动资产加动负债(一般倩况大于一) 速动则=(流动资产?存货)爲动负债(酸性实验比率) 现金t淳=现金僦动负债 流动性比率是短期债权人关心的,趣高越好;但对公司而言f高流动性比率意味着流动性好,或者现金等短期资产运用效率低下。对于一家拥有强大借款能力的公司?看似较低的流动性比率可能并非坏的信号 2。(财隽杠轩扌旨标) 负债=(总资产?总权益)/总资产Or (长期负债+流动负债)/总资产 权益乘数=总资产/总权益=1 +负债权益比 利息倍数=EBlT/SJ 息 现金对利息的保障倍数(CaSh COVerage radio) = EBrrDa/利息 ≡。资产管理或资金周转指标 存货周转率=产品销售成本府货存货周转天数=365天府货周转率 应收账款周转率=(赊)销售额/应收账款 总资产周转率=销售额/总资产=1虑本密集度 4盈利性mt示 销售利润率=净利润/f肖售额 资产收益率ROA =净利润/总资产 权益收益率ROE =净利润/总权益 5。市场价tag量指标 市盈率=每股价格/每股收益EPS其中EPS=净利润/发行股票数

第一章导论 1. 公司目标:为所有者创造价值公司价值在于其产生现金流能力。 2. 财务管理的目标:最大化现有股票的每股现值。 3. 公司理财可以看做对一下几个问题进行研究: 1. 资本预算:公司应该投资什么样的长期资产。 2. 资本结构:公司如何筹集所需要的资金。 3. 净运营资本管理:如何管理短期经营活动产生的现金流。 4. 公司制度的优点:有限责任,易于转让所有权,永续经营。缺点:公司税对股东的双重课税。 第二章会计报表与现金流量 资产 = 负债 + 所有者权益(非现金项目有折旧、递延税款) EBIT(经营性净利润) = 净销售额 - 产品成本 - 折旧EBITDA = EBIT + 折旧及摊销 现金流量总额CF(A) = 经营性现金流量 - 资本性支出 - 净运营资本增加额 = CF(B) + CF(S) 经营性现金流量OCF = 息税前利润 + 折旧 - 税 资本性输出 = 固定资产增加额 + 折旧 净运营资本 = 流动资产 - 流动负债 第三章财务报表分析与财务模型 1. 短期偿债能力指标(流动性指标) 流动比率 = 流动资产/流动负债(一般情况大于一) 速动比率 = (流动资产 - 存货)/流动负债(酸性实验比率) 现金比率 = 现金/流动负债 流动性比率是短期债权人关心的,越高越好;但对公司而言,高流动性比率意味着流动性好,或者现金等短期资产运用效率低下。对于一家拥有强大借款能力的公司,看似较低的流动性比率可能并非坏的信号 2. 长期偿债能力指标(财务杠杆指标) 负债比率 = (总资产 - 总权益)/总资产 or (长期负债 + 流动负债)/总资产 权益乘数 = 总资产/总权益 = 1 + 负债权益比 利息倍数 = EBIT/利息 现金对利息的保障倍数(Cash coverage radio) = EBITDA/利息 3. 资产管理或资金周转指标 存货周转率 = 产品销售成本/存货存货周转天数= 365天/存货周转率 应收账款周转率 = (赊)销售额/应收账款 总资产周转率 = 销售额/总资产 = 1/资本密集度 4. 盈利性指标 销售利润率 = 净利润/销售额 资产收益率ROA = 净利润/总资产 权益收益率ROE = 净利润/总权益 5. 市场价值度量指标 市盈率 = 每股价格/每股收益EPS 其中EPS = 净利润/发行股票数 市值面值比 = 每股市场价值/每股账面价值 企业价值EV = 公司市值 + 有息负债市值 - 现金EV乘数 = EV/EBITDA 6. 杜邦恒等式 ROE = 销售利润率(经营效率)x总资产周转率(资产运用效率)x权益乘数(财杠) ROA = 销售利润率x总资产周转率 7. 销售百分比法 假设项目随销售额变动而成比例变动,目的在于提出一个生成预测财务报表的快速实用方法。是根据资金各个项目与销售收入总额的依存关系,按照计划销售额的增长情况预测需要相应追加多少资金的方法。 d = 股利支付率 = 现金股利/净利润(b + d = 1) b = 留存比率 = 留存收益增加额/净利润 T = 资本密集率 L = 权益负债比 PM = 净利润率 外部融资需要量EFN(对应不同增长率) = ?销售额 销售额 ×(资产?自发增长负债) ?PM×预计销售额×(1?d) 8. 融资政策与增长 内部增长率:在没有任何外部融资的情况下公司能实 现的最大增长率ROA×b 1?ROA×b 可持续增长率:不改变财务杠杆的情况下,仅利用内 部股权融资所..率ROE×b 1?ROE×b 即无外部股权融资且L不变 P×b×(L+1) T?P×b×(L+1) 可持续增长率取决于一下四个因素: 1. 销售利润率:其增加提高公司内部生成资金能力,提高可持续增长率。 2. 股利政策:降低股利支付率即提高留存比,增加内部股权资金,提高..。 3. 融资政策:提高权益负债比即提高财务杠杆,获得额外债务融资,提高..。 4. 总资产周转率:提高即使每单位资产带来更多销售额,同时降低新资产的需求.. 结论:若不打算出售新权益,且上述四因素不变,该

112公司理财计算题 第二章:财务比率的计算 (一)反映偿债能力的指标 1、资产负债率= 资产总额负债总额×100% =所有者权益 负债长期负债 流动负债++×100%(资产=负债+所有者权益) 2、流动比率= 流动负债 流动资产 ×100% 3、速动比率= 流动负债速动资产×100% =流动负债待摊费用 存货预付账款流动资产---×100% 4、现金比率= 流动负债 短期投资短期有价证券货币资金现金) ()(+×100% (二) 反映资产周转情况的指标 1、应收账款周转率= 平均应收账款余额赊销收入净额=2 --÷+期末应收账款)(期初应收账款销售退回、折让、折扣 现销收入销售收入 2、存货周转率= 平均存货销货成本=2 ÷+期末存货)(期初存货销货成本 习题: 1、某公司20××年末有关财务资料如下:流动比率=200%、速动比率=100%、现金比率=50%、流动 负债 = 1000万元,该公司流动资产只包括货币资金、短期投资、应收账款和存货四个项目(其 中短期投资是货币资金的4倍)。要求:根据上述资料计算货币资金、短期投资、应收账款和存 货四个项目的金额。 2、某公司20××年末有关财务资料如下:流动比率=200%、速动比率=100%、现金比率=20%、资产负债率=50%、长期负债与所有者权益的比率为25%。要求:根据上述资料填列下面的资产负债表简表。 资 产 负 债 表(简) 390万元,

本年度销售收入为680万元(其中现销收入480万元,没有销售退回、折让和折扣),销货成本 为560万元。要求:根据上述资料计算应收账款周转率和存货周转率。 4、某公司20××年度全年销售收入为600万元,其中现销收入为260万元,没有销售退回、折 让和折扣,年初应收账款为30万元,年末应收账款比年初增加了20%,则应收账款周转率应该是多少? 5、某公司20××年度全年销货成本为400万元,年初存货为50万元,年末存货比年初增加了20%, 则存货周转率应该是多少? 第三章:货币时间价值 1、单利:终值F n=P·(1+i·n) 【公式中i为利率,n为计息期数】 现值P = F n/(1+i·n) 2、复利:终值F n= P·CF i,n= P·(1+i)n 【公式中(1+i)n 称为复利终值系数,简写作CF i,n】 现值P= F n·DF i,n=F n/(1+i)n【公式中1/(1+i)n 称为复利现值系数,简写作DF i,n】3、年金:终值F n= R·ACF i,n【公式中ACF i,n是年金终值系数的简写,R为年金,n为年金个数】 现值P = R·ADF i,n【公式中ADF i,n 是年金现值系数的简写】 习题: 1、某公司从银行取得贷款600000元,年利率为6%,按复利计息,则5年后应偿还的本利和共 是多少元?(CF0.06,5 =1.338,DF0.06,5=0.747) 2、某公司计划在5年后以600000元更新现有的一台设备,若年利率为6%,按复利计息,则现 在应向银行存入多少钱?(CF0.06,5 =1.338,DF0.06,5=0.747) 3、某公司计划在10年内每年年末将5000元存入银行,作为第10年年末购买一台设备的支出, 若年利率为8%,则10年后可积累多少资金?(ACF0.08,10=14.487,ADF0.08,10=6.710)4、某人计划在10年中每年年末从银行支取5000元以备零用,若年利率为8%,现在应向银行 存入多少钱?(ACF0.08,10=14.487,ADF0.08,10=6.710) 5、某公司现在存入银行一笔现金1000000元,年利率为10%,拟在今后10年内每年年末提取 等额现金作为职工奖励基金,则每年可提取多少现金?(ACF0.1,10=15.937, ADF0.1,10=6.145)

Chapter 30 Financial Distress Multiple Choice Questions 1. Financial distress can be best described by which of the following situations in which the firm is forced to take corrective action? A. Cash payments are delayed to creditors. B. The market value of the stock declines by 10%. C. The firm's operating cash flow is insufficient to pay current obligations. D. Cash distributions are eliminated because the board of directors considers the surplus account to be low. E. None of the above. 2. Insolvency can be defined as: A. not having cash. B. being illiquid. C. an inability to pay one's debts. D. an inability to increase one's debts. E. the present value of payments being less than assets. 3. Stock-based insolvency is a: A. income statement measurement. B. balance sheet measurement. C. a book value measurement only. D. Both A and C. E. Both B and C. 4. Flow-based insolvency is: A. a balance sheet measurement. B. a negative equity position. C. when operating cash flow is insufficient to meet current obligations. D. inability to pay one's debts. E. Both C and D.

Assets =Liabilities + Stockholders’ Equity Assets =(Current + Fixed)Assets Net Working Capital= Current Assets–CurrentLiabilities Revenues — Expenses =Ine Salesor Revenues(-)Cost of goodssold(=)Grossprofit毛利(—) Administrative/marketingcosts行政管理/营销成本, Depreciation折旧(=) Oper ating Profit营业利润(—)Interests, Taxes (=)Net ine净收益(-) Dividends to preferred stocks(=)Earning available to mon shareholders Cash Flow From Assets(CFFA) =Cash Flow to Creditors+ Cash Flow to S tockholders Cash Flow From Assets = Operating Cash Flow营运现金流量–NetCapitalSpending净资本支出–Changes in NWC净营运资本得变化 OCF (I/S)营运现金流=EBIT息税前利润+ depreciation –taxes =$547 NCS净资本支出(B/S and I/S)= endingnet fixedassets–beginningnet fixed assets + depreciation = $130 Changes inNWC(B/S)=ending NWC –beginning NWC=$330 CFFA = 547 –130 – 330 = $87 CF to Creditors (B/S and I/S) = interest paid – net new borrowing = $24 CF to Stockholders (B/S andI/S)= dividends paid – net new equity raised= $63 CFFA= 24 +63=$87 Current Ratio流动比率= CA /CL2,256/ 1,995 =1、13times QuickRatio 速动比率= (CA – Inventory)/ CL (2,256 – 301)/ 1,995 =、98 times CashRatio 现金比率= Cash / CL 696/ 1,995 = 、35times NWC to Total Assets = NWC /TA (2,256– 1,995)/5,394=、05 Interval Measure区间测量=CA /averagedaily operatingcosts 2,256 / ((2,006+1,740)/365)= 219、8days Total DebtRatio资产负债率= (TA –TE)/TA (5,394 – 2,556) /5,394=52、61% Debt/Equity资本负债率=TD /TE(5,394–2,556)/ 2,556=1、11 times Equity Multiplier权益乘数=TA /TE = 1 +D/E 1+1、11 =2、11 Long-term debt ratio长期债务率= LTD / (LTD+ TE) 843/(843+2,556)=24、80% Times Interest Earned利息保障倍數= EBIT息税前利润EarningsBeforeInterest and Tax/Interest 1,138/ 7= 162、57times CashCoverage现金涵盖比率= (EBIT+ Depreciation)/ Interest (1,138 + 116)/ 7= 179、14times InventoryTurnover存货周转= Cost of GoodsSold/ Inventory 2,006 /301 =6、66 times Days’ Salesin Inventory 销售库存得天数= 365/ InventoryTurnover

第1篇概论 第1章公司理财导论 1.1复习笔记 公司的首要目标—股东财富最大化决定了公司理财的目标。公司理财研究的是稀缺资金如何在企业和市场内进行有效配置,它是在股份有限公司已成为现代企业制度最主要组织形式的时代背景下,就公司经营过程中的资金运动进行预测、组织、协调、分析和控制的一种决策与管理活动。从决策角度来讲,公司理财的决策内容包括投资决策、筹资决策、股利决策和净流动资金决策;从管理角度来讲,公司理财的管理职能主要是指对资金筹集和资金投放的管理。公司理财的基本内容包括:投资决策(资本预算)、融资决策(资本结构)、短期财务管理(营运资本)。 1.资产负债表 资产负债表是总括反映企业某一特定日期财务状况的会计报表,它是根据资产、负债和所有者权益之间的相互关系,按照一定的分类标准和一定的顺序,把企业一定日期的资产、负债和所有者权益各项目予以适当排列,并对日常工作中形成的大量数据进行高度浓缩整理后编制而成的。资产负债表可以反映资本预算、资本支出、资本结构以及经营中的现金流量管理等方面的内容。 2.资本结构 资本结构是指企业各种资本的构成及其比例关系,它有广义和狭义之分。广义资本结构,亦称财务结构,指企业全部资本的构成,既包括长期资本,也包括短期资本(主要指短期债务资本)。狭义资本结构,主要指企业长期资本的构成,而不包括短期资本。通常人们将资本结构表示为债务资本与权益资本的比例关系(D/E)或债务资本在总资本中的构成(D/A)。准确地讲,企业的资本结构应定义为有偿负债与所有者权益的比例。 资本结构是由企业采用各种筹资方式筹集资本形成的。筹资方式的选择及组合决定着企业资本结构及其变化。资本结构是企业筹资决策的核心问题。企业应综合考虑影响资本结构的因素,运用适当方法优化资本结构,从而实现最佳资本结构。资本结构优化有利于降低资本成本,获取财务杠杆利益。 3.财务经理

月度公司理财工作总结 为切实加强应收账款的催收工作,加大应收账款的催收力度, 本月集团公司对理财公司的内部机构进行了重新设置,将理财公司划分为四个科,即综合科和三个清欠业务科,同时充实了理财公司的领导力量。 为进一步加强内部管理,保障各科工作的顺利、协调开展,理 财公司着手制定了各科科长及工作人员岗位责任制,将责任层层落实,做到各尽其能,各负其责。同时,建立完善了档案资料借阅登记制度、会议记录纪要制度、发送文件签收制度、月度联席会议制度等各项管理措施,用制度进行管理,使各项工作的开展有条不紊、井然有序。 现将一个月来理财公司工作情况汇报如下: 一、资产管理 1、废旧物资处理:本月理财公司对烧成车间废耐火砖,机修废铁屑,物资公司废油桶组织了集中招标处理。共收回资金19573.40元。 2、闲置资产: ①配合有关部门办理**闲置房拍卖事宜:因集团公司决定对公 司在**的闲置房屋进行处置,为此,理财公司先期与**市的一些房屋中介公司、拍卖公司进行了接触、咨询,将了解的情况上报公司后,公司领导决定先拿两套闲置房进行拍卖,即**花园一套,**苑一套。随即,理财公司着手进行实质性操作。经总工程师室、评标办和理财公司共同了解、对比,选定**拍卖公司作为拍卖方。该公司实力较为

雄厚,费用收取合理(成交额的1%,且流标。其它拍卖公司则收取 成交额的3%~5%)。随后,又协同拍卖公司人员到房屋进行实地勘测、拍照,并对房屋进行了评估。 ②办理**闲置房出租事宜:与**科技公司签订了房屋(**大厦)续租合同。 ③对闲置房进行管理:对**的5套公司没有钥匙的闲置房安排 进行了门锁的更换。 二、应收账款的催收 理财公司自成立业务科以来,催款人员在各业务科长的带领下,熟悉情况,掌握资料,迅速展开所负责片区的催收工作。业务一科主要对**分公司所属的**建筑队、**经贸公司等前期有询证结果的十家欠款单位进行了清理和催收,并与其中有些单位达成意向性还款协议。业务二科通过前阶段拉网式的调查摸底,对**片区的欠款单位情况已心中有数。本月重点对其中有催收价值的20余家单位进行了资料完 备和实地催收。催回欠款1.2万;确认债权依据55万;重点跟踪了 **公司、**、**实业等单位。业务三科继续保持对**、**招待所、**经贸委、**国道等重点单位的跟踪催收,本月又从**招待所催回欠款5万元。他们通过对本科业务的现状分析,拟将**片区作为下一步的清欠工作方向。在分别征求了集团公司各相关业务部门的意见后,三科(本"月工作总结"由:jiaokedu.)提交了对**片区党政机关需询 证核实的欠款单位名单一份报送公司领导,并、充实完备了**片区三

(P/F,10%,1)=0.9091 (P/A,10%,3)=2.4869 (P/F,10%,5)=0.6209 (P/A,10%,4)=3.1699 (P/F,10%,6)=0.5645 第一章导论 1. 公司目标:为所有者创造价值公司价值在于其产生现金流能力。 2. 财务管理的目标:最大化现有股票的每股现值。 3. 公司理财可以看做对一下几个问题进行研究: 1. 资本预算:公司应该投资什么样的长期资产。 2. 资本结构:公司如何筹集所需要的资金。 3. 净运营资本管理:如何管理短期经营活动产生的现金流。 4. 公司制度的优点:有限责任,易于转让所有权,永续经营。缺点:公司税对股东的双重课税。 第二章会计报表与现金流量 资产= 负债+ 所有者权益(非现金项目有折旧、递延税款) EBIT(经营性净利润)= 净销售额- 产品成本- 折旧 EBITDA = EBIT + 折旧及摊销 现金流量总额CF(A) = 经营性现金流量- 资本性支出- 净运营资本增加额= CF(B) + CF(S) 经营性现金流量OCF = 息税前利润+ 折旧- 税 资本性输出= 固定资产增加额+ 折旧

净运营资本= 流动资产- 流动负债 第三章财务报表分析与财务模型 1. 短期偿债能力指标(流动性指标) 流动比率= 流动资产/流动负债(一般情况大于一) 速动比率= (流动资产- 存货)/流动负债(酸性实验比率) 现金比率= 现金/流动负债 流动性比率是短期债权人关心的,越高越好;但对公司而言,高流动性比率意味着流动性好,或者现金等短期资产运用效率低下。对于一家拥有强大借款能力的公司,看似较低的流动性比率可能并非坏的信号 2. 长期偿债能力指标(财务杠杆指标) 负债比率= (总资产- 总权益)/总资产or (长期负债+ 流动负债)/总资产 权益乘数= 总资产/总权益= 1 + 负债权益比 利息倍数= EBIT/利息 现金对利息的保障倍数(Cash coverage radio) = EBITDA/利息 3. 资产管理或资金周转指标 存货周转率= 产品销售成本/存货存货周转天数= 365天/存货周转率 应收账款周转率= (赊)销售额/应收账款 总资产周转率= 销售额/总资产= 1/资本密集度 4. 盈利性指标 销售利润率= 净利润/销售额 资产收益率ROA = 净利润/总资产 权益收益率ROE = 净利润/总权益

Chapter 20 Issuing Securities to the Public Multiple Choice Questions 1. An equity issue sold directly to the public is called: A. a rights offer. B. a general cash offer. C. a restricted placement. D. a fully funded sales. E. a standard call issue. 2. An equity issue sold to the firm's existing stockholders is called: A. a rights offer. B. a general cash offer. C. a private placement. D. an underpriced issue. E. an investment banker's issue. 3. Management's first step in any issue of securities to the public is: A. to file a registration form with the SEC. B. to distribute copies of the preliminary prospectus. C. to distribute copies of the final prospectus. D. to obtain approval from the board of directors. E. to prepare the tombstone advertisement. 4. A rights offering is: A. the issuing of options on shares to the general public to acquire stock. B. the issuing of an option directly to the existing shareholders to acquire stock. C. the issuing of proxies which are used by shareholders to exercise their voting rights. D. strictly a public market claim on the company which can be traded on an exchange. E. the awarding of special perquisites to management.

{财务管理公司理财}公司理财知识点总结

提纯率=再投资率=留存收益增加额/净利润=1-股利支付率 资本密集率=资产总额/销售收入 4.内部增长率=(ROAXb)/(1-ROAXb) 可持续增长率=ROE/(1-ROEXb):企业在保持固定的债务权益率同时没有任何外部权益筹资的情况下所能达到的最大的增长率。是企业在不增加财务杠杆时所能保持的最大的增长率。(如果实际增长率超过可持续增长率,管理层要考虑的问题就是从哪里筹集资金来支持增长。如果可持续增长率始终超过实际增长率,银行家最好准备讨论投资产品,因为管理层的问题是怎样处理所有的这些富余的现金。) 1.增长率的决定因素 利润率、股利政策(提纯率)、筹资政策(财务杠杆)、总资产周转率 2.如果企业不希望发售新权益,而且它的利润率、股利政策、筹资政策和总资产周转率(资 本密集率)是固定的,那么就只会有一个可能得增长率 3.如果销售收入的增长率超过了可持续增长率,企业就必须提高利润率,提高总资产周转 率,加大财务杠杆,提高提纯率或者发售新股。 第六章. 1.贷款的种类:纯折价贷款、纯利息贷款、分期偿还贷款 纯折价贷款:国库券(即求现值即可) 纯利息贷款:借款人必须逐期支付利息,然后在未来的某时点偿还全部本金。 如:三年期,利率为10%的1000美元纯利息贷款,第一年第二年要支付1000X0.1的利息,第三年末要支付1100元。 分期偿还贷款:每期偿还利息加上一个固定的金额。其中每期支付的利息是递减的,而且相等总付款额情况下的总利息费用较高。

第7章 1.市场对某一债券所要求的利率叫做该债券的到期收益率。 2.如果债券低于或高于面值的价格出售,则为折价债券或溢价债券。 折价:票面利率为8%,市场利率(到期收益率)为10% 溢价:票面利率为8%,市场利率为6%(投资者愿意多支付价款以获得额外的票年利息) 3.债券的价值=票面利息的现值+面值的现值(与利率呈相反变动) 4.利率风险:债券的利率风险的大小取决于该债券的价格对利率变动的敏感性。其他条件相同,到期期限越长,利率风险越大;其他条件相同,票面利率越低,利率风险越大。 5.债券的当期收益率是债券的年利息除以它的价格。折价债券中,当期收益率小于到期收益率,因为没有考虑你从债券折价中获取的利得。溢价相反。 6.公司发行的证券:权益性证券和债务证券。 7.权益代表一种所有权关系,而且是一种剩余索取权,对权益的支付在负债持有人后。拥有债务和拥有权益的风险和利率不一样。 8.债务性证券通常分为票据、信用债券和债券。长期债务的两种主要形式是公开发行和私下募集 9.债务和权益的差别: 1.债务并不代表公司的所有权的一部分。债权人通常不具有投票权。 2.公司对债务支付的利息属于经营成本,因此可以再税前列支,派发给股东的股利则不能抵税。 3.未偿还的债务是公司的负债。如果公司没有偿还,债权人对公司的资产就有合法的索取权。这种行为可能导致两种可能的破产:清算和重组。 4.债券合约是公司和债券人之间的书面协议,有时也叫做信用证书,里面列示了债券的各种