Study Notes of

Standards and Practice Handbook

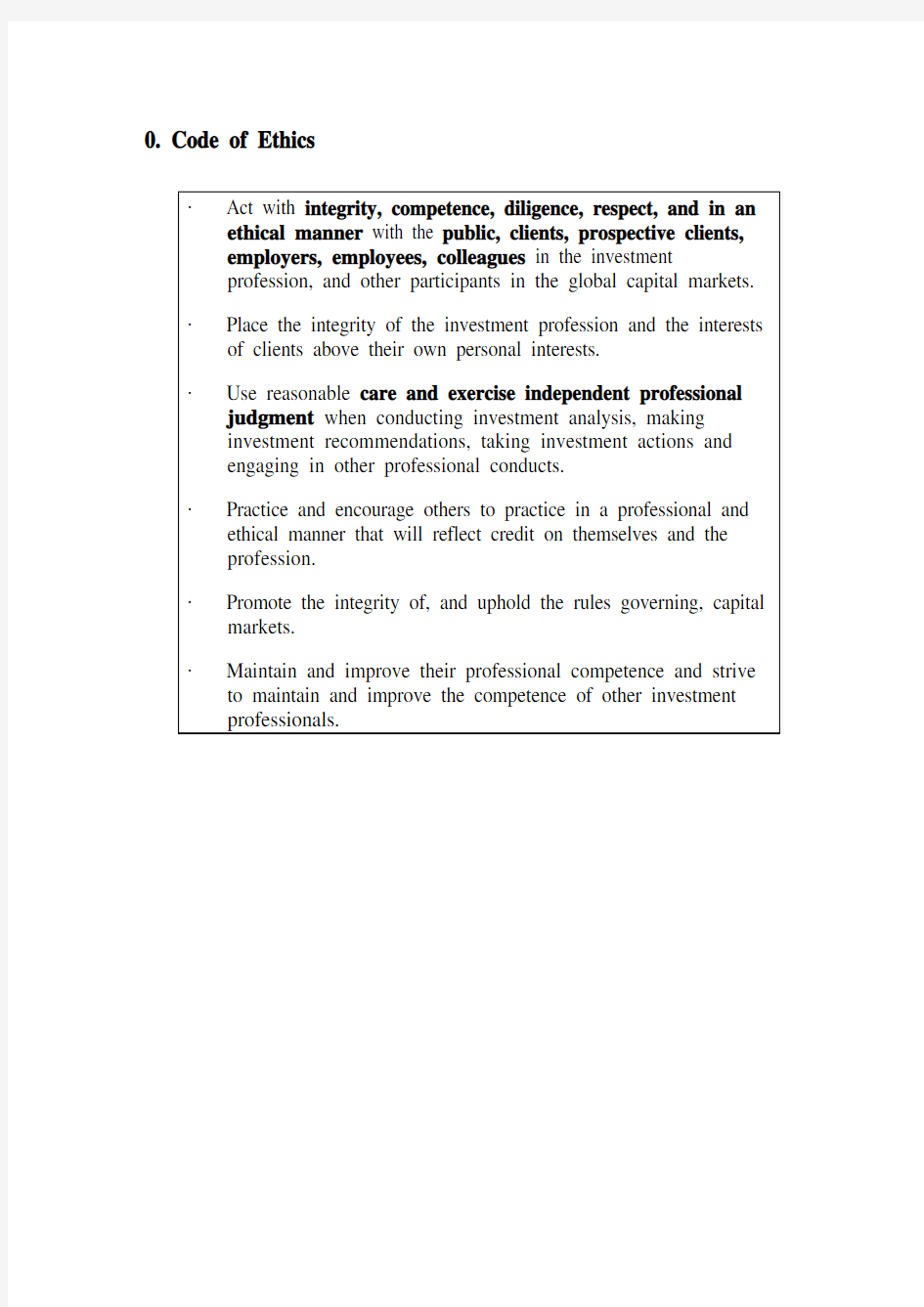

0. Code of Ethics

·Act with integrity, competence, diligence, respect, and in an ethical manner with the public, clients, prospective clients,

employers, employees, colleagues in the investment

profession, and other participants in the global capital markets.

·Place the integrity of the investment profession and the interests of clients above their own personal interests.

·Use reasonable care and exercise independent professional judgment when conducting investment analysis, making

investment recommendations, taking investment actions and

engaging in other professional conducts.

·Practice and encourage others to practice in a professional and ethical manner that will reflect credit on themselves and the

profession.

·Promote the integrity of, and uphold the rules governing, capital markets.

·Maintain and improve their professional competence and strive to maintain and improve the competence of other investment

professionals.

I.Professionalism

A. Knowledge of law

B. Independent and Objectivity

C. Mispresentation

D. Misconduct

Offer gift/benefit/compensation etc. to compromise independence is violation.

C&S (Codes and Standards) do not require reporting to the government regulatory organizations for violations or CFAI for potential violations (but it’s encouraged).

Advices from legal counsel do not absolve M&C (Members and Candidates) from requirement to comply.

Best ways: report to supervisor (first time), dissociate (if necessary later).

Company paid trip should be strictly for business.

Modest gifts/entertainment is OK, but should be careful. Gift from customer is OK, but all accepted need to be disclosed.

Working with IBD is appropriate only when conflicts are adequately and effectively managed and disclosed.

No corporate issuer should reimburse M&C for air transportation.

Frequent meeting should be paid attention to.

Non-flat fee related to security performance should not be accepted.

Factual Information from recognized and statistical reporting services need not be cited.

Knowingly means either knows or should have known.

Chartroom is also included in communication related to Misrepresentation.

If performance guarantee is built in to the structure of the product itself or institution’s agreement to cover loss, M&C can tell customers.

Author and publisher should both be mentioned.

Must not misrepresent abilities.

Oral communications should also avoid plagiarism.

Misrepresent by unintentionally error is not a violation, but should be corrected and related parties should be informed once found.

Source of plain-language s should also be acknowledged.

Risk relaying on second-hand information should be avoided-best way: obtain a copy from original source.

Misconduct is related to M&C’s professional life, mostly related to dishonesty.

Personal beliefs usually do not cause a violation.

Any words like luxury high-level, etc from company should be a violation.

Reporting can be treated as dissociation.

Both offer and solicit benefit is a violation.

Oral communication can also violate plagiarism.

Flight and hotel paid by covering company is acceptable.

Government bond still have interest rate risk, so guarantee should be carefully expressed.

II.Integrity of capital markets

A. Material nonpublic information

B. Market manipulation

Material non-public information: change in auditor certification or no longer qualified; government reports of economic trends (before published).

Less reliable & more ambiguous, less material,

Not necessary to wait for the slowest method to delivery information.

Aware of information selectively disclosed.

Briefing or conference call / disclose to only analyst cannot be called public.

Guidance or interpretation of public information may be material & non-public.

Mosaic theory: should save and document the research.

Report of famous analyst (may influence the market) is a kind of material non-public before published.

“Looking over firewall” need approval.

Sometimes prohibition to avoid using material non-public can tell out, at this time, take only the contra side of unsolicited customer trades.

Fail to prevent transfer and misuse of material non-public is a violation.

If the impact of an information is unknown (such as the direction of price change cannot be predicted), it is not considered material.

Unreliable information could not be considered.

Market manipulation: Prices & Volume; Transaction based & Information based.

Transaction based: manipulate the security itself; manipulate an instrument to control derivatives.

Trading for tax purpose is not prohibited, such as selling and immediately buying back.

Using inaccurate/misleading information may cause market manipulating.

The best action when heard material nonpublic information is to promote public disclosure.

Legal disputes and government economic trends report can be material nonpublic before disclosed.

The departure of the fund manager is not material.

If a client who has material nonpublic information makes an trade order based on that, M&C should decline.

III.Duties to clients

A. Loyalty, Prudence and Care

B. Fair dealing

C. Suitability

D. Performance presentation

E. Preservation of confidentiality

The client of pension plans or trusts is the beneficiaries of them.

Clients who are unaware of the recommendation change should be advised before the contrary order accepted.

Determining suitability should base on the characteristics of entire portfolio, not issue-by-issue analysis.

Voting proxies should be made sure according to the interests of the client, both fail to vote or vote too much to save cost might be violation.

Proxy voting policy should be disclosed.

If uncertain of clients action, ask; if in doubt, disclose in written and obtain client’s approval.

Terminated accounts should be included in performance presentation.

Deleting an asset from recommendation list is also a recommendation change.

Illegal information of clients could be relayed only to proper authorities.

While CFAI investigates clients’ confidential information, analyst should offer.

The clients’ investment purpose is confidential (even for charity).

M&C need disclose strategy, but not specific trades if they agree with strategy.

Firms can offer different levels of services (different in depth but not priority) as long as this is disclosed to all clients.

Disseminate new recommendations should be based on suitability and known interest, not all clients.

Limit the number of people who are privy to the fact that a recommendation is going to be disseminated.

Process executing orders in first-in first-out order (Don’t confuse with inventory accounting).

Disclose trade allocation procedures (it can be asymmetric only due to the different need of clients).

If clients withhold information, suitability analyst can’t be complete but must be done based on provided information; thus, M&C are responsible only for assessing

suitability.

M&C who manage pooled assets to a specific mandate are not responsible to the suitability of the share purchasers.

Pay attention of the material changes in clients’ situations to confirm if there’s any suitability change.

Providing confidential information to CFAI’s Professional Conduct Program (PCP) is not a violation.

Passing confidential information to authorized employees/colleagues is permitted.

The word equal is not necessary in fair dealing, or it may violate suitability.

M&C can not be the client of himself.

Soft dollar arrangement is required to be disclosed only if it causes conflict or potential conflict.

Annual inquiry of client’s situation is required.

It is applicable law, not Code and Standard that decides whether illegal activity of client should be reported to authorities.

Authorized fellow employee can be disclosed confidential information.

Only pro-rata allocation of IPO is permitted.

Sitting in the board should be disclosed to both employer and clients.

Generally offering to do a client’s information update through mail is not sufficient to comply with Suitability.

A recommendation list can be sent without regard to suitability.

Soft dollar must be used for the benefit of clients, but is not required for the exact client.

Charging different fee for same service violates the Fair Dealing.

Ask someone to help to “introduce” non-complete or biased performance is a violation.

IV.Duty to employers

A. Loyalty

B. Additional compensation arrangements

C. Responsibility of Supervisors

The clients’ investment purpose is confidential (even for charity).

It’s not required to put employer’s interests ahead of family and other personal obligations; it should be discussed and balanced.

With non-compete agreement absence, S&M can contact old clients if not using contact list from old employee but the memory himself or public information.

Accepting addition jobs with no conflic t with employee do not need permission.

Supplemental & contingent compensation arrangement from clients should be reported in written to employer and obtain consent.

While company has no proper compliance procedures,M&C should decline supervisory responsibility in writing.

Even rejected material is the property of the employer.

The additional compensation from clients should be disclosed to employer, but the disclosure to other clients is not M&C’s duty.

Cheating the employer is not related to DUTY TO EPLOYER.

Accepting additional compensation should be disclosed to and obtain written consent from all parties involved.

Delegation of supervisory responsibility does not relieve the duty of supervisor.

If appropriate code and action failed to stop violation, the supervisor is not in violation.

Once a violation is discovered, supervisor should increase supervision or place appropriate limitation on the wrongdoer.

After termination form the employer, soliciting clients is no longer a violation.

CEO is not necessary to be the supervisor of the employee.

Undertaking independent practice is required to disclose and obtain written consent only to&from employer.

The preparation of independent activity or leaving the employer is not required to be disclosed.

V.Investment Analysis, Recommendations, and Action

A. Diligence and reasonable basis

B. Communication with clients and perspective clients

C. Record retention

If a member does not agree a group’s views which have been worked out in reasonable procedure and base, he does not necessarily remove his name from the

report, but have to document a notice.

By periodically checking the reasonable base, third-party research can be used for investment recommendation.

M&C must keep existing clients informed with respect to changes to the choice of investment process on an ongoing basis.

Without other standards, CFAI recommends at least 7 years of Record Retention.

While working in new company, M&C can recreate models used before by only knowledge and recreate supporting documents at the same time.

Using the research result of the firm is not lack of diligence and reasonable unless there’s a reason to believe the basis is questionable.

Detailed information must be available (and availability disclosed) while brief recommendation is offered.

VI.Conflicts of Interest

A. Disclosure of conflicts

B. Priority of transactions

C. Referral fees

Conflicts can be exist between clients, employer and self.

Power to vote or direct the voting is a kind of interest.

Special compensation from employer might be conflict with client’s interest, should be disclosed.

Disclose must be made prominently, only disclose in footnote is not enough.

Only when the investment decision that causes conflict is determined should the disclosure be made.

There should be black out periods prior to trades for clients to prevent manage of front running.

Job offer or potential is a kind of conflict source.

The beneficial owning of security by immediate relative is a conflict, but non-immediate is not.

VII.Responsibilities as a CFAI Member or CFA Candidate

A. Conducts as M&C in the CFA program

B. Reference to CFAI, the CFA Designation, and CFA

Program

Cheating in any examination is a violation.

Expressing opinion or beliefs concerning CFAI or CFA program is not inhibited.

Using CFA committee position to benefit self is a violation.

Members must sign PCS (Professional Conduct Statement) & pay dues annually.

CFA related sign must used either after the name or as adjectives (not nouns).

M & C have the right to express his/her opinion of CFA and CFA plan even if it’s negative opinion.

Annual conduct report is an obligation of Members.

“Highest ethical standard” is permitted to describe CFA.

CFA一级和二级难度对比 来源:浦江.财经 6月份的CFA考试已经过去,但大家的备考脚步却不能停止,毕竟CFA有三个级别,只有考完了并通过了三级后,你才可以如释重负。对于CFA三级而言,一级、二级为选择题会给人错觉是不是通过会很简单了?这是个很错误的想法,CFA考试不会是简单的,就一级、二级难度也是很大的。那么浦江.财经就这两个级别难度对比来说明。 一、从学习内容看 CFA二级虽然在知识领域上和一级基本重合,但对理解深度的要求则比一级高很多,而且题目设置的技术难度也有明显提升。如果说CFA考生通过死记硬背概念和一定的考试技巧,或许是可以侥幸通过CFA一级的考试。但是当你面临二级的考试时,它所考核的偏重就在于综合应用了。 这时候,考生需要将一、二两个级别的考试内容结合在一起。考生在备考的时候,学会理解以后还要进行活学活用。所以,通过CFA二级考试需要的是真才实学。 二、从知识点内容看 其实,CFA二级考试具体的考试内容还是和一级差不多的那几个科目。但是,知识点变零散了,而且没有一级那么明显的系统化。在考生的备考过程中,知识点的理解、梳理和运用,都需要考生自己去总结,去发现各个章节和各个知识点之间的联系:也就是融会贯通。 三、从出题模式看 CFA一级考试全是单项选择题,上下半场各有120道。每道题目各自独立,互不影响。二级考试上下半场各只有60道题,出题形式则是一篇短文附带一组问题。问题之间很多是前后相关;一旦对整体文意把握不准,或者前一题做错,那么后一题做错的几率就陡然升高。

四、难度总结 CFA一级考试:难度在于计算和零散知识点的记忆,同时强调记忆和计算,所以考生在复习和考试的过程中极容易遇到陌生的知识点,在复习的时候对教材的逻辑难于把握和整理。比如理解基本的经济分析方法和常识,基本的金融市场运行实践(指数计算,股票内在价值DDM 计算的基本公式,财务报表分析技术),考卷也考察对某些重要计算公式的理解(比如正态分布的性质、对单尾或者双尾检验的理解,经济学的MC、MP的计算过程理解和图形分析,债券的久期和凸性等)。所以广大考生在复习一级考试的时候,要着重对整体框架把握的基础上,通过后面大量做题再对单个零散知识点进行把握,做到复习的时候心中有数把握框架,做题的时候注重细节。 CFA二级考试:越来越侧重于对题干中信息量的把握、每个LOS的串联记忆还有对计算信息量得筛选。二级之所以难度较高,还在于二级考试考察理解和运用,而非单纯的记忆。所以我们在复习二级考试的过程中,应该淡化一些基本公式的死记硬背(如定量分析还有衍生品中的一些公式),重点应该在于理解每个章节的框架还有每个知识点的内在含义,这样在做题的过程中才能有的放矢,对每个案例中的信息进行有效的检索、筛选,提高自己的阅读能力还有对题目所给的信息的检索能力。

CFA一级考试知识点 第八部分固定收益证券 债券五类主要发行人 超国家组织supranational organizations,收回贷款和成员国股金还款 主权(国家)政府sovereign/national governments,税收、印钞还款 非主权(地方)政府non-sovereign/local governments(美国各州),地方税收、融资、收费。 准政府机构quasi-governments entities(房利美、房地美) 公司(金融机构、非金融机构)经营现金流还款 Maturity到期时间、tenor剩余到期时间 小于一年是货币市场证券、大于一年是资本市场证券、没有明确到期时间是永续债券。 计算票息需要考虑付息频率,未明确的默认半年一次付息。 双币种债券dual-currency bonds支付票息时用A货币,支付本金时用B货币。 外汇期权债券currency option bongds给予投资人选择权,可以选择本金或利息币种。 本金偿还形式 子弹型债券bullet bond,本金在最后支付。也称为plain vanilla bond(香草计划债券) 摊销性债券amortizing bond,分为完全摊销和部分摊销。 偿债基金条款sinking found provision,也是提前收回本金的方式,债券发行方在存续期间定期提前偿还部分本金,例如每年偿还本金初始发行额的6%。 票息支付形式 固定票息债券fixed-rate coupon bonds,零息债券会折价发行,面值与发行价之差就是利息,零息债券也称为纯贴现债券pure discount bond。

高顿CFA一级考试复习备考技巧分享 CFA一级考试复习备考技巧简述 1.所有知识点和公式要做到烂熟于胸。 2.制定合理的学习时间进度表并严格按照计划进行学习复习,CFA考试的准备过程是对考生耐力和意志力的考验,建议考生严格按照制定的学习计划进行学习复习。 给予考生的建议: 考生应根据自身专业背景和金融基础详细制定学习计划 每周约10至15小时,共约18周进行CFA的学习 每个session至少需一周时间学习 临考前预留四到六周时间反复操练习题并进行模拟考试 考试前两个学习日强化公式记忆 3. 在认真学习完一遍Study Notes后,学员应根据自身情况及LOS的要求,找出考试要点、难点,逐个攻破。 每个Study session的学习内容都是自成体系,考生可分科目进行复习,总结各科目的理论、公式,经典题及难题。在深入理解各科知识点的基础上,再将整个知识体系融会贯通,全面性、条理性、逻辑性地把握知识要点。 4. 抓住三个重点 从考试内容比重来看,FSA, Equity,Corporate Finance以及Fixed Income占分较多,考生应侧重学习。 FSA部分在实际考试中很强调对不同accounting method的理解,其中LIFO,FIFO的对比,Revenue recognition方式的使用范围,及对Financial ratio的影响,Operating/Capital lease财务比率对比等内容每年必考。FSA部分是CFA 考试通过的关键。如果时间和精力有限,建议从这部分先开始看,Corporate Finance在学习过程中由于知识点较为连贯,是CFA一级考试比较容易拿分的部分,建议考生牢固掌握WACC,DDM,CAPM等知识重点,保证考试时的答题正确率。 5.熟练掌握公式和概念间的互动关系 CFA一级考试题量大,时间短,因为建议考生在理解性记忆的基础上强制性记忆。例如:LIFO和FIFO对Net Income,cash flow的影响,在考场上没有时间去一步步推导它们之间的关系,而是一下就能想到在物价水平不变和上升的市场环境中,使用LIFO的现金流相对于FIFO方法要偏大,真正做到将公式和互动关系烂熟于胸。 6. 模拟做题至关重要 答题速度是通过CFA一级考试的关键。CFA考试是对考生能力和体力的双重考核,试想一个从没跑过一万米的人去参加一万米比较,成绩可想而知。模拟做题的目的在于巩固学习成果,提高做题速度,找出薄弱环节并弥补学习的不足之处。 7.建议考生参加专业课程培训 CFA是一张综合能力证书,其备考过程就是知识积累,能力培养的过程,变专业知识为个人实际能力才是投资CFA考试的最大收益。CFA一级考试的所有知识点在随后的二级三级考试中都会被要求综合应用。CFA一级学习如果

关于CFA一级的各个重点 前语:下面就详细说说每门科目的复习要点吧,其实简而言之就是道德放最后,抓财报和道德两个大头(共35%),CFA学习一定要有方向,不要太杂。 关于每门的要点: 1.数理方法(比重12%,难度B) 一上来首先应该看这门,这章会详细说到计算器的用法,这样看后面几门也会方便些,这门注意下什么是MAD,CV,连续复利计算,critical value,p-value,两种假设检验的错误,4种抽样方法的不同,parametric tests 和unparametric tests,还有年金的计算就差不多了。不过要小心年金的计算,是不是先付年金等等,这边计算起来还是要格外小心的~~~我考试的时候感觉这部分是比较简单的,基本上1分钟1题,在刚刚结束道德的摧残后,做到这里感觉格外舒心~~哈哈 2.经济学(比重10%,难度B-) 个人认为是CFA1级里最简单的一门,可能在第一轮准备的时候并不觉得,不过真到最后就会发现,其它科目知识点虽然简单但是庞杂得很,只有这门,只要抓住精髓,考试的时候简直是轻松的很。这门需要注意:什么是MC,MB,MP,MRP,等各种M的东西,所有者和消费者surplus部分要认真理解下,何为资源分配的有效,各种事情对surplus,MC,MB的影响,对于各种曲线,分清楚长期和短期,公司和行业,线移动的因素,何处交点为最佳,何处交点最有效,何处是surplus,各种效应,D,MB,MR的关系,wage rate的准确含义,还有一个很重要的就是LAS,SAS和AD的影响因素(这点几乎是这门后半部分的精髓)~~~~我考试的时候这门写的最轻松写意,平均半分钟一题就画过去了~~~ 3.财务报表分析(比重20%,难度E) 没悬念的,这部分是1级的重点也是难点,再怎么强调多多复习这部分也不为过 主要知识点有: Session 7 主要讲的IFRS 和U.S. GAAP在不同情况下的区别,还有各种statements 的元素构成。 Session 8 就是集中在Income statement, Balance Sheet, Cash flow statement 和各种Ratio analysis。这一章节需要注意知识点是Revenue & Expense recognition, Basic and Dilute EPS, Goodwill;Trading, Holding to maturity and Available for sale securities, 然后cash flow statement中重点要会Direct & Indirect method, 以及两者之间的相互转化。Ratio analysis中需要注意ROE中Basic & Extended DuPont equation以及四大Ratio: Activity, Liquidity, Solvency and Profitability ratios。 Session 9 这部分是个硬骨头,真的不好啃,知识点也是灰常灰常集中。 ⅰ. Inventories这一小节中,需要懂得inventory valuation method 在IFRS和GAAP 两种准则下的库存定价方式,然后是FIFO/LIFO对报表中四大ratio的影响,接下来就要熟练地将基于LIFO会计假设的报表数据转化成基于FIFO的情况,了解LIFO reserve 和LIFO liquidation。 ⅱ. Long-lived Assets中首先要了解Capitalization & Expense 对net income, stockholder’s equity, cash flow 以及对四大financial ratios的影响,然后就是software development and research & development,Depreciation method, Asset retirement obligation对ratios的影响。最后要注意的就是虚幻的goodwill了,Impairment of

CFA一级职业伦理道德重点考点汇总 原创S. 诚明智库Finance 2017-05-16 金融改变世界学习创富人生 点击题目下方蓝字关注诚明智库Finance 1431316505675053465.jpg 对于职业伦理道德一定不能忽视,因为其向来是CFA一级和CFA二级考试的重点之一,尤其是CFA一级中职业伦理道德所占比例高达15%。在CFA考试中,涉及到职业道德与专业行为标准的考题往往最先出现。迅速并准确解答这部分考题,不仅有助于从考试开始就建立起信心,也能提高通过考试的机率,所以本文要说的职业伦理道德学习方法就对这些考生很重要了。 CFA一级职业伦理道德学习避免误区 第一个误区:CFA道德与标准是死规定,死准则。因此,只要我记住每条准则就能应付考试; 在CFA考试中,考生绝不会碰见以下具有中国特色的题型:请问,CFA道德与专业行为标准第2条准则的第1条细则是什么?如果CFA协会也走中国特色,按照这样的思路来出题,我们相信不久以后,中国将会成为全球CFA考试通过率最高的国家。然而,CFA协会考查候选人(candidates)是否掌握CFA道德与标准的重要原则是:运用(Applications)。每道CFA考题都是一个有针对性和典型的案例。考生需要在富有工作生活借鉴的案例情景中做出正确判断。仅仅知道每条准则的具体内容,却不熟悉每条准则的运用,并不能帮助候选人顺利通过CFA考试,更谈不上成为一名合格的投资分析师。 第二个误区:CFA是投资分析师考试,道德与标准在今后工作中的实际作用不大。因此,掌握别的科目,比如股票分析等知识,更实际更重要。这导致许多考生把道德与标准的学习安排在临考前复习冲刺的最后阶段。 CFA道德与标准在金融投资行业的运用其实非常广泛。在微观层面,公司建立严格,清晰的道德与专业行为标准能确保员工向客户提供规范而满意的投资服务,同时也能帮助员工正确处理工作中常遇见的道德困境(Ethical dilemmas)。在宏观层面,通过鼓励企业遵守行业道德与专业行为标准,有助于提高整个金融市场的诚信和有效运作。因此我们看到,不仅很多国家持续出台新的法律法规来完善金融市场,而且很多公司也建立起内部监管机制,比如防火墙(firewall, 也称Chinese wall),来规范员工专业行为和服务质量,从而提升企业信誉。 CFA一级职业伦理道德学习的重点考点 1.Mr.J 生于A国(户籍所在国)工作于B国(工作地所在国)若相关规定有如下严苛强弱程度排序:A国相关法律规定 CFA一级知识点总结 Ethics 部分 Objective of codes and standard:永远是为了maintain public trust in 1.Financial market 2.Investment profession 6个code of ethics 1.Code 1—ethics and pertinent d persons a. 2.Code 2---primacy of client’s interest a.Integrity with investment profession b.客户利益高于自身利益 3.Code 3---reasonable and independent a.必须注意reasonable care b.必须exercise independent professional judgment---必须独立判断! 4.Code 4---ethical culture in the profession a.不但自己要practice,而且要鼓励别人practice—不仅仅是自己一个人去做, 要所有人共同去做 5.Code 5---ethnical culture in the capital market! a.促进整个capital market的integrity,推广其相关法规---增强公众对资本市 场的trust! b.Capital market是基于 i.Fairly pricing of risky assets; ii.Investors‘ confidence 6.有关competence—能力---competence 7个standard of professional conduct 1.Standard 1---professionalism---knowledge of law a.不需要成为法律专家,但是必须understand和comply with applicable law; b.当两个law发生conflict,则要遵守更加严格的法律! c.Knowingly---know or should know d.必须attempt to stop the violation,如果不能stop,then must dissociate from the violation!必须从其中分离出去! i.Remove name from the written report; ii.Ask for a different assignment e.并不要求向有关部门report!(do not require) f.向CFA 进行书面报告report--encouraged to so 全球最大的CFA(特许金融分析师)培训中心 总部地址:上海市虹口区花园路171号A3幢高顿教育 电话:400-600-8011网址:https://www.doczj.com/doc/ce7999680.html, 微信公众号: gaoduncfa 1 CFA 一级考试知识点总结 CFA 一级考试知识点总结 Security-market Indexes 1. Price-weighted index=sum of Stock price/#of Stock inthe index adjusted for split a. 价格高的股票对该股指的影响大! b. DJIA 和日经指数Nikkei 都是价格加权指数! c. 必须考虑股票分割的影响! 2. Market value-weighted index=sum[price for today#ofshares outstanding]/sum[price for base year#of shares outstanding]*base year index value a.其不足之处是大的Market capitalization 的公司对指数的影响大! b.Value-weighted 市场价值加权指数会自动的调整了股票分割对指数的影响! c.S&P is market value-weighted index d.NYSE is market value-weighted index e.NASDAQ is market value-weighted index 3. Unweighted index---直接将每只股票的收益相加求算术平均数或者几何平均数 a.首先计算出各个股票的收益率;---可能有正有负; b.计算其算术平均数或者几何平均数—注意几何平均数的计算方法 各位考生,CFA 备考已经开始,为了方便各位考生能更加系统地掌握考试大纲的重点知识,帮助大家充分备考,体验实战,高顿网校开通了全免费的CFA 题库(包括精题真题和全真模考系统),题库里附有详细的答案解析,学员可以通过多种题型加强练习,通过针对性地训练与模考,对学习过程进行全面总结。 2018年CFA一级衍生品科目复习攻略 今天CFA小编为大家奉上衍生品(Derivatives)这门课,在CFA考试中占比5%,比重较小,但内容不是很难,算是可以答满分的科目,所以大家一定要好好把握哦。 CFA一级衍生品包括3个reading,比较重要的是Reading 58:Basics of Derivative Pricing and Valuation. CFA小编总结了各个reading的重要考点: Reading 57:Derivative Markets and Instruments(金融衍生品市场及工具)金融衍生品的定义;金融衍生品市场的分类及区别;金融衍生品的分类;金融衍生品的优缺点; Reading 58:Basics of Derivative Pricing and Valuation(金融衍生品基本定价和估值原理) 金融衍生品定价的基本原理;区别远期和期货合约的定价以及估值;合约期初、期中、期末如何计算远期的价值,以及理解影响远期价值的因素;解释期货和远期定价的异同;解释互换和远期定价的不同;欧式期权价值的计算以及影响因素;欧式期权的平价公式、远期平价公式以及二叉树模型的理解;美式期权与欧式期权定价的差异。 Reading 59:Risk Management Applications of Option Strategies(风险管理应用:期权策略) 看涨期权和看跌期权的到期价值、利润、最大/小盈亏、盈亏平衡点的计算;Covered call和protective put的到期价值、利润、最大/小盈亏、盈亏平衡点的计算; 好啦,小编来拎拎衍生品里的干干货啦!敲黑板啦!必考!:衍生品的基本分类,交易所市场和OTC市场之间的区别,了解Forward, Futures, Option, Swap的特征,辨析远期和期货的异同,远期利率协议(FRA),期权定价的影响因素,期权平价公式(Put –Call Parity),一期二叉树模型,期权的风险管理策略(Covered Call & Protective Put)。 衍生品不算简单,但是题目难度不难,所以该拿A的拿A,千万别手软,这部分拿A还是非常不难的哈!加油啦!同学们 文章来源:泽稷网校 高顿网校CFA 2013年CFA一级数量方法备考概论 高顿教育旗下品牌:高顿网校 年的考纲变化 2013年的考纲变化 2013 ?数量方法(Quantitative Methods)2013年与2012年的考纲基本一致,没有大的变化。 近两年考情分析 1.占考试比重12%左右。 2.知识点比较分散,需要全面掌握。 3.要熟记各类公式。 4.计算题以基本概念为主,要熟练掌握计算器的使用。 考试需要掌握的具体内容Reading LOS 5.货币的时间价值a)interpret interest rates as required rate of return, discount rate, or opportunity cost; b)explain an interest rate as the sum of a real risk-free rate, and premiums that compensate investors for distinct types of risk; c)calculate and interpret the effective annual rate, given the stated annual interest rate and the frequency of compounding; d)solve time value of money problems for different frequencies of compounding; e)calculate and interpret the future value (FV) and present value (PV) of a single sum of money, an ordinary annuity, an annuity due, a perpetuity (PV only), and a series of unequal cash flows; f)demonstrate the use of a time line in modeling and solving time value of money problems. CFA一级:NOTES教材上的重点 在备考CFA一级时,高顿小编想说说关于CFA考试教材Notes和CFA考试重点问题 1.cfa考试的notes用背下来吗?不用的话需要看到什么程度才能通过考试? 观点:不用背下来。CFA考察的是考生是否已经掌握了知识点,不是考政治经济学。五本NOTES一般整套看下来需要多遍,因人而异,看到打开目录中的LOS,每看一个LOS都能简单说出LOS中的精华即可,对于一些模棱两可的知识点,务必回到书本上仔细再看。 通常第一遍看完还不是特别懂。往往按顺序读完了最后的Alternatives,你就把前面的economics, quantitative通通忘掉了,有点像“转碟子”的杂技,不断的让碟子重新转动起来才是最后的成功。这种情况不妨可以开始做题。NOTES中的题目有点偏难,主要是“偏”,不过知识点差不多一样,可以对着书本,开卷考试做一套,没压力,还知道了知识点是如何变成考题的。 等你题目从头到尾做了120道题,彻底觉得再一打开目录中的LOS就知道每个LOS要点。就算程度达到了。剩下的就是不断的模考再模考。CFA考试资料 2.考试重点在哪能找到,什么时候能出考试重点? 观点:其实没什么考试重点。 考试是以一个一个部分出现的,你看看下面这同学的成绩单: Multiple Choice --fail Q# Topic Max Pts <=50% 51%-70% >70% - Alternative Assets 12 - - * - Derivatives 12 * - - - Economics 24 * - - - Equity Analysis 24 * - - - Ethical 36 - * - - Financial Statemen 68 - * - - Fixed Income 24 - * - - Portfolio 12 - - * 转:金融分析师(CFA)一级考试课本总结- Financial Statement Analysis 阅读(375) 评论(0) 发表时间:2008年12月21日07:27 本文地址:https://www.doczj.com/doc/ce7999680.html,/blog/657383549-1229815661 本文标签: turnover income equity Statement sales Financial Statement Analysis FS被investor和creditor有用,还有gov regulator,tax authority和其他,提供short-term liquidity, long-term earning power, growth opportunity和asset position of the firm. 还应该是relevent,timely,reliable,material和consistent允许time-series和cross- sectional 比较。 The Financial Account Standards Board(FASB)是美国的,建立了Generally Accepted Accounting Principle(GAAP) The International Organization of Securiies Commission(IOSC)建立跨过的disclosure标准 The International Accounting Standards Board(IASB)目标是提供international uniformity, 虽然没有执行力,但很多国家还是采用IASB GAAP 除了Balance sheet,income statement和statement of cash flow,分析师还应该看financial statement footnotes,statement of comprehensive income,statement of stockholders’ equity,proxy statement,supplementary schedules和management dicision and analysis(MD&A). 独立auditor有doubts,就说qualified opinion;auditor能提供reasonable assurance证明报表没有material misstatement,就说unqualified revenue和expense在earn和incur时候就实现了,不管cash flow是什么时候。matching principle要求expense在revenue实现的同时记录。 实现revenue的条件,completion of the earning process和assuance of payment 实现revenue的方法,sale basis method,percentage-of-completion method,completed contract method, installment sales method,cost recovery method unusual or infrequent items: 是pre-tax 在net income from continuing operations之前。线上gains of losses from 关掉business segment gains of losses from 下属公司卖assets or investments provisions for environmental remediation impairments, write-offs, write-downs 和restructuring costs integration expense 跟收购有关 Extrodinary items: 是net of taxes 在net income from continuing operation 之后。线下losses from expropriation of assets uninsured losses from natural disasters discontinued operation:是管理层决定dispose of但还没做或当年没做,在operation已经有income或者loss之后。必须在实质上与公司别的活动不一样。是net of tax,在线下accounting change,累积效应,是after tax basis在线下,通常不需要restate 历史,除非: 1. 库存会计方法改变 2.改变(to/from)full-cost method, 比如油气开采 3.改变(to/from)percentage-of-completion method 4.IPO前的任何改变 操纵earnings和managerial discretion,4种操纵方法: 1.classification of good/bad news, 好消息放在线上,坏消息放在线下 Chartered Financial Analyst CFA 一级考试知识点总结Stanhope CFA一级知识点总结 Ethics 部分 Objective of codes and standard:永远是为了maintain public trust in 1.Financial market 2.Investment profession 6个code of ethics 1.Code 1—ethics and pertinent d persons a. 2.Code 2---primacy of client’s interest a.Integrity with investment profession b.客户利益高于自身利益 3.Code 3---reasonable and independent a.必须注意reasonable care b.必须exercise independent professional judgment---必须独立判断! 4.Code 4---ethical culture in the profession a.不但自己要practice,而且要鼓励别人practice—不仅仅是自己一个人 去做,要所有人共同去做 5.Code 5---ethnical culture in the capital market! a.促进整个capital market的integrity,推广其相关法规---增强公众对 资本市场的trust! b.Capital market是基于 i.Fairly pricing of risky assets; ii.Investors‘ confidence 6.有关competence—能力---competence 7个standard of professional conduct 1.Standard 1---professionalism---knowledge of law a.不需要成为法律专家,但是必须understand和comply with applicable law; b.当两个law发生conflict,则要遵守更加严格的法律! c.Knowingly---know or should know d.必须attempt to stop the violation,如果不能stop, then must dissociate from the violation!必须从其中分离出去! i.Remove name from the written report; ii.Ask for a different assignment 2020年CFA一级考试延期,考生的备考时间延长了半年,有了充足的时间去准备,那么都有哪些备考资料是要 学习的呢? 1、CFA官方教材 CFA官方教材在报名注册时购买的,针对CFA全三级考试每级都有6本,每本都不同,是由权威的教授编著的,针对整个CFA知识点的掌握,CFA官方教材是一套专业的书籍。CFA官方教材分为电子版与纸质版两种,纸质版要另外掏钱! 2、CFA道德手册 CFA考试道德部分很重要,考试只看study notes内的道德是不足的,一定还要看道德手册 3、CFAmock 官方免费提供一套Sample和一套Mock。虽然价格不菲,但这些样题的难度和实际考试相当,是notes模拟题所不能比拟的,因此一定要做,并且在做题过程中应多多揣测出题人的思路和意图。 4、CFAnotes study notes是以CFA协会每年公布的考纲为基础编写的,尤其是对于CFA一级考试来说。CFA notes绝对是效率最高的备考资料,其中涵盖了99%的知识点。总结复习要点,但缺陷就是忽略了内在逻辑,对于CFA一级考试来说,则完全够用。如果考生对于CFA notes中的知识点有理解不到位的地方,可以辅之以CFA官方教材详细查看。 5、CFA官方考纲 每年CFA协会都会更新CFA考纲,会对CFA考试科目的权重及知识点有所删减更改。例如2018年CFA考纲变动为25%,由此高顿CFA建议根据CFA协会公布的考纲选择最新的备考资料来学习。 6、CFA计算器使用教程 CFA协会只允许考生使用两种计算:德州仪器的BA II Plus(or Professional)以及惠普的12C(or Platinum)。这两种计算器一般平时很少接触,而且使用复杂,建议考生提前熟练,在考场上节省时间 7、CFA词汇表 CFA考试作为全英考试,对于中国考生来说是个不小的挑战,尤其是一些专业的金融单词。 8、CFA公式表QuickSheet CFA考试的时候,不会给出公式的,公式都是需要自己背诵下来,考试不允许带与教材相关的学习资料,CFA考 试常用公式表。 9、网课、历年真题 也可以参加CFA培训机构的课程,提供视频网课、直播课程、历年真题以及习题库练习。 第1页 全球最大的CFA(特许金融分析师)培训中心 总部地址:上海市虹口区花园路171号A3幢高顿教育 电话:400-600-8011 网址:https://www.doczj.com/doc/ce7999680.html, 微信公众号:gaoduncfa 1 CFA 一级考试重点:Due Diligence and Reasonable basis 关于CFA 一级重点,罗列一个关于Due Diligence and Reasonable basis 试题 A model expert developed a model. He gathered lots of historical data, which shows unilateral bull market, that is, only upward trend. If he made investment suggestions based on these historical data, is he in violation of the Code and Standards? A. No B. Yes, because he should combine more of other theories to make decision. C. Yes, because he should also simulate more of the downward trend. Solution: C The model expert violated the Code and Standards V(A) Diligence and Reasonable Basis by making investment suggestions based only on historical data which shows only upward trend. The proper way to avoid violating Standards is to simulate more of the downward trend also. 各位考生,2015年CFA 备考已经开始,为了方便各位考生能更加系统地掌握考试大纲的重点知识,帮助大家充分备考,体验实战,高顿网校开通了全免费的CFA 题库(包括精题真题和全真模考系统),题库里附有详细的答案解析,学员可以通过多种题型加强练习,通过针对性地训练与模考,对学习过程进行全面总结。 CFA一级考试各科目介绍及重点解析 在CFA考试过程当中,许多考生都在自学的过程中走过些许弯路。对往年的重点着重观望,对教材中仅有十几页的科目内容可能只是扫视几遍便匆匆翻篇。为那些常年标着五角星的CFA重点刻苦钻研。这样的备考方法并没有错,然而随着这几年CFA考试协会的出题更新,越来越多的考生反映,在实际考试当中会出现作为边角边料的小细节知识点出现。 偶偶考生们会此类题目打住考试的节奏,满脑袋转悠也只有稍许浅薄的印象。针对历年变化的CFA考试,高顿财经CFA研究中心为考生们整理了在CFA一级考试中,经常会考到的一些重难点。希望考生可以通过此类难点的归纳,调整自己的备考计划。 CFA一级考试中十大科目考试重点介绍: 职业伦理: 提高从业人员的职业和道德素养,特别是国际上对受托人的责任的要求,降低了公司内部人员职业违规方面的风险,同时提升公司内部的整体职业素养,由此提高公司整体的管治。 数量分析: 定量分析就是以数量工具测算投资组合关联性,概率统计,为设定合理理性的投资规划提供技术支撑。在一级二级考试中是考试占比比较大的考试科目,考察金融分析中的一些常用的计算方法。 经济学: 经济学课程以经典宏观、微观经济学内容讲解弹性、价格曲线、生产者剩余、消费者剩余、垄断和市场形态,宏观金融政策和中央银行等知识,让考生了解经济运行的宏观和微观经济知识。 财务报表分析: 财务报表是一级二级的考试重点,内容涉及三大会计报表,现金流量测控,养老会计、管理会计、税收规避FACC 等会计术语,考试难度不大,并且现在的考核方式更加灵活。一级二级中财务报表是重点科目,占比考试20%左右的权重,权重较大。 公司理财: 公司理财详细的介绍了资本的成本,使公司规划出最合适的资本结构,来获得资本的最优收益。在制定资本预算时,可做出正确的现金流量估计和风险分析,从而作出正确的决定。在决定股利政策时,充分了解其中的资讯和意义。深入地了解如何实现公司融资结构与投资结构的最优化。 权益类投资分析: 权益证券分析详细介绍了上市、集资时的定价流程,在收购合并时该付出多少。也可在评估过程中了解行业的前景,从而作出正确的商业决定。以及并购行动中,如何合理评估企业的价值。 CFA一级重点难点解析1 1、FIFO、LIFO那点事 FIFO真实反映了存货价值,对B/S更适用。LIFO真实反映了COGS,对I/S更合适。 两种方法的差异是考试重点。假设存货价格上升(inflation)且存货数量稳定或上升,LIFO将导致生产成本上升,所得税下降,现金流上升,净利润(税前&税后收益)下降,期末存货余额。简而言之,明确LIFO计价下,生产成本和现金流是存货价格同向变化,其他指标反向变化。FIFO的各项影响是与LIFO相反。 我们应该明确认识存货价格上升时,LIFO因COGS较高而享受tax advantage,以低估存货资产作为代价。而一旦收入不佳,还可以采用LIFO liquidation遮掩颓势,其舞弊原理在于使用老久存货降低COGS,从而操作net income上升,粉饰损益表。存货价格上升时,FIFO因COGS较低同事唱红B/S,I/S表,即使近期存货成本上升短期内也不一定影响I/S表美观,但长期可能悄悄将利润掏空。 考生要从时点、持续经营的会计期间的角度比较和理解LIFO和FIFO的财务影响,到底谁才是真正的保守计量存货方式,洞穿存货计价这点事儿。 2、CFO直接法与间接法的异曲同工 直接法是从I/S的每一个主体出发,主体包括:和客户相关的销售收入(cash collection from customers),供应商相关的购买存货现金支出(cash outflow to purchases),公司运营相关的费用(operating expenses),债主相关的利息支出(interest expenses),政府相关的税收支出(taxes expense)。这些主体在B/S里也有相对应的项目,计算每一个主体现金流的时候先做流量处理→接着资产的增加是现金的减少,负债的增加是现金的增加。按照这样的顺序把每一个主体的现金流确认后,再计算总额。 间接法是从I/S表的net income开始,先调整I/S里的non-cash charge,比如depreciation,amortization→再调整I/S里不是由于经营性活动产生的现金流(non-operating items),一般是减去处置固定资产的利得,加上处置固定资产的损失→最后调整B/S下的由于权责发生制引起的CA和CL,得到CFO。 虽然直接法计算CFO的起点从I/S表的销售收入开始,而间接法计算CFO的起点是从I/S表中的“底部”净收益开始的,但是最终二种方法对CFO的计算结果完全一致。且报表呈现直接法,footnotes里面呈现间接法。 直接法与间接法只有在计算CFO的时候才会出现。且考试中如果是计算请先判断到底使用哪一种方法计算CFO,之后再去寻找条件。尤其是间接法在题目没有给予NI,depreciation的时候,知道用勾稽公式去计算(勾稽公式的整理会在“难点突破课程”中总结讲解)。如果是分析题,必须要非常熟悉权责发生制和收付实现制的本质区别,题目灵活,需要有比较稳定和扎实的基础。 不论是计算CFO的直接法和间接法,还是分析公司的earning quality都是考试中必然出现的考点,考生要引起高度重视。 3、当固定资产属于投资性质的时候 固定资产在计量原则上都使用historical cost model,且未来相应的发生折旧或者减值。但是一旦固定资产属性发生变化,从自有的固定资产转变成了投资性质固定资产(也就成为了金融资产的性质)后,从理论上是应该让investment property可以随行就市来体现公司资产的经济现实。可是U.S.GAAP和IFRS处理是不同的。 U.S.GAAP下没有将investment property和其他长期固定资产做区分,言下之意就是仍然用cost model来计量。IFRS下,investment property是指能带来租金收入或资本增值和能同时产生这两种收益的资产,而当investment property的FV能可靠计量时,可以采取cost或FV计量模式。所谓的FV model就是随行就市,将一个固定资产可以看似AFS来处理,因为产品性质属于可供出售。也如同AFS,如果upward,那么FV surplus就记录在equity部分;不同的是如果downward,这部分损失依照会计的谨慎原则,直接记录进I/S。假设从owner-occupied转换成Investment property(也就是cost model转换成FV model),就当做revaluation处理。其唯一的原则就是只要是loss就按照谨慎原则进入I/S,而gain的话都进入equity,作为revaluation surplus。那么有人会问,假设先FV先CFA一级知识点总结

CFA一级考试知识点总结

2018年CFA一级衍生品科目复习攻略

CFA考试一级金融数量分析

CFA一级:NOTES教材上的重点

(CFA)一级考试课本总结 - Financial Statement Analysis

CFA一级知识点总结最全

2020年CFA一级备考资料有哪些

CFA一级考试重点:Due Diligence and Reasonable basis

CFA一级考试各科目介绍及重点解析

CFA一级重点难点解析1

相关主题

文本预览