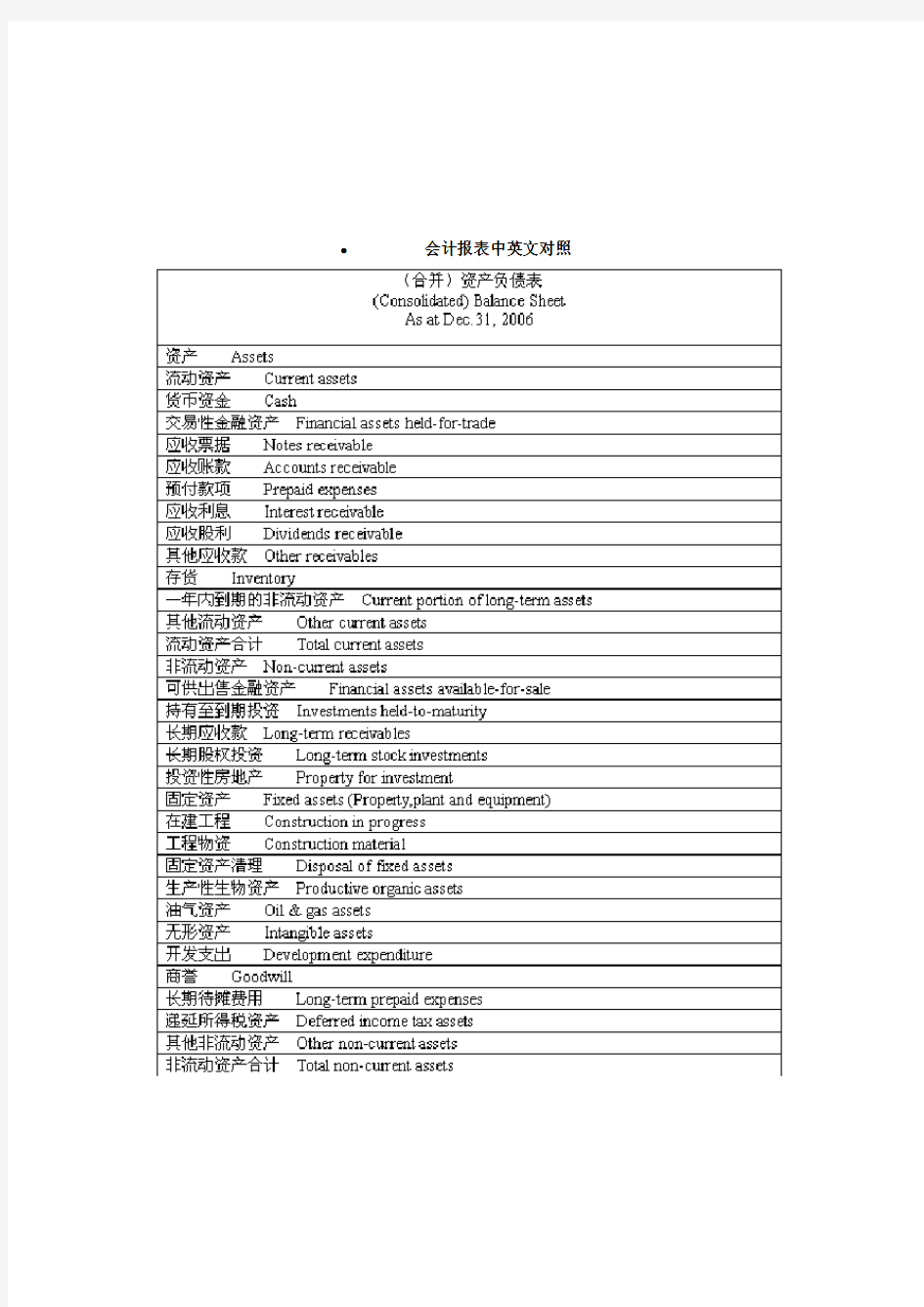

?会计报表中英文对照

Accounting

1. Financial reporting(财务报告) includes not only financial statements but also other means of communicating information that relates, directly or indirectly, to the information provided by a business enterprise’s accounting system----that is, information about an enterprise’s resources, obligations, earnings, etc.

2. Objectives of financial reporting: 财务报告的目标

Financial reporting should:

(1) Provide information that helps in making investment and credit decisions.

(2) Provide information that enables assessing future cash flows.

(3) Provide information that enables users to learn about economic resources, claims against those resources, and changes in them.

3. Basic accounting assumptions 基本会计假设

(1) Economic entity assumption 会计主体假设

This assumption simply says that the business and the owner of the business are two separate legal and economic entities. Each entity should account and report its own financial activities.

(2) Going concern assumption 持续经营假设

This assumption states that the enterprise will continue in operation long enough to carry out its existing objectives.

This assumption enables accountants to make estimates about asset lives and how transactions might be amortized over time.

This assumption enables an accountant to use accrual accounting which records accrual and deferral entries as of each balance sheet date.

(3) Time period assumption 会计分期假设

This assumption assumes that the economic life of a business can be divided into artificial time periods.

The most typical time segment = Calendar Year

Next most typical time segment = Fiscal Year

(4) Monetary unit assumption 货币计量假设

This assumption states that only transaction data that can be expressed in terms of money be included in the accounting records, and the unit of measure remains relatively constant over time in terms of purchasing power.

In essence, this assumption disregards the effects of inflation or deflation in the economy in which the entity operates.

This assumption provides support for the "Historical Cost" principle.

4. Accrual-basis accounting 权责发生制会计

5. Qualitative characteristics 会计信息质量特征

(1) Reliability 可靠性

For accounting information to be reliable, it must be dependable and trustworthy. Accounting information is reliable to the extend that it is:

Verifiable: means that information has been objectively determined, arrived at, or created. More than one person could consider the facts of a situation and reach a similar conclusion.

Representationally faithful: that something is what it is represented to be. For example, if a machine is listed as a fixed asset on the balance sheet, then the company can prove that the machine exists, is owned by the company, is in working condition, and is currently being used to support the revenue generating activities of the

company.

Neutral: means that information is presented in accordance with generally accepted accounting principles and practices, and without bias.

(2) Relevance 相关性

Relevant information is capable of making a difference in the decisions of users by helping them to evaluate the potential effects of past, present, or future transactions or other events on future cash flows (predictive value) or to confirm or correct their previous evaluations (confirmatory value).

(3) Understandability 可理解性

Understandability is the quality of information that enables users who have a reasonable knowledge of business and economic activities and financial reporting, and who study the information with reasonable diligence, to comprehend its meaning.

(4) Comparability 可比性

Comparability: suggests that accounting information that has been measured and reported in a similar manner by different enterprises should be capable of being compared because each of the enterprises is applying the same generally accepted accounting principles and practices.

Consistency: suggests that an entity has used the same accounting principle or practice from one period to another, therefore, if the dollar amount reported for a category is different from one period to the next, then chances are that the difference is due to a change like an increase or decrease in sales volume rather than being due to a change in the method of calculating the dollar amount. (5) Substance over form 实质重于形式

Substance over form emphasizes the economic substance of an event even though its legal form may provide a different result.

It requires that business enterprise should perform accounting recognition, measurement and reporting in accordance with the economic substance rather than the legal form of an event or transaction.

(6) Materiality 重要性

Information is material if its omission or misstatement could influence the resource allocation decisions that users make on the basis of an entity’s financial report. Materiality depends on the nature and amount of the item judged in the particular circumstances of its omission or misstatement. Deciding when an amount is material in relation to other amounts is a matter of judgment and professional expertise.

(7) Conservatism 谨慎性

Conservatism dictates that when in doubt, choose the method that will be least likely to overstate assets and income, and understate liabilities and expenses.

(8) Timeliness 及时性

Timeliness means having information available to decision makers before it loses its capacity to influence decisions. If information becomes available only after the time that a decision must be made, it has no capacity to influence that decision and thus lacks relevance.

6. Basic accounting elements 基本会计要素

(1) Asset 资产

An asset is a resource that is owned or controlled by an enterprise as a result of past transactions or events and is expected to generate economic benefits to the enterprise.

(2) Liability 负债

A liability is a present obligation arising from past transactions or events which are expected to give rise to an outflow of economic benefits from the enterprise.

A present obligation is a duty committed by the enterprise under current circumstances. Obligations that will result from the occurrence of future transactions or events are not present obligations and shall not be recognized as liabilities.

(3) owners’ equity 所有者权益

Owners’ equity is the residual interest in the assets of an enterprise after deducting all its liabilities.

Owners’ equity of a company is also known as shareholders’ equity.

(4) Revenue 收入

Revenue is the gross inflow of economic benefits derived from the course of ordinary activities that result in increases in equity, other than those relating to contributions from owners.

(5) Expense 费用

Expenses are the gross outflow of economic benefits resulted from the course of ordinary activities that result in decreases in owners’ equity, other than those relating to appropriations of profits to owners.

(6) Profit 利润

Profit is the operating result of an enterprise over a specific accounting period. Profit includes the net amount of revenue after deducting expenses, gains and losses directly recognized in profit of the current period, etc.

7. Five measurement attributes 会计计量属性

(1) Historical cost 历史成本

Assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given to acquire them at the time of their acquisition. Liabilities are recorded at the amount of proceeds or assets received in exchange for the present obligation, or the amount payable under contract for assuming the present obligation, or at the amount of cash or cash equivalents expected to be paid to satisfy the liability in the normal course of business.

(2) Current replacement cost 现时重置成本

Assets are carried at the amount of cash or cash equivalents that would have to be paid if a same or similar asset was acquired currently. Liabilities are carried at the amount of cash or cash equivalents that would be currently required to settle the obligation.

(3) Net realizable value 可实现净值

Assets are carried at the amount of cash or cash equivalents that could be obtained by selling the asset in the ordinary course of business, less the estimated costs of completion, the estimated selling costs and related tax payments.

(4) Present value 现值

Assets are carried at the present discounted value of the future net cash inflows that the item is expected to generate from its continuing use and ultimate disposal. Liabilities are carried at the present discounted value of the future net cash outflows that are expected to be required to settle the liabilities within the expected settlement period.

(5) Fair value 公允价值

Assets and liabilities are carried at the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.

8. Financial statements 财务报表

(1) Balance sheet 资产负债表

A balance sheet is an accounting statement that reflects the financial position of an enterprise at a specific date.

(2) Income statement 损益表

An income statement is an accounting statement that reflects the operating results of an enterprise for a certain accounting period.

(3) Statement of cash flows 现金流量表

A cash flow statement is an accounting statement that reflects the inflows and outflows of cash and cash equivalents of an enterprise for a certain accounting period.

(4) Statement of changes in owners’equity 所有者权益变动表

A statement of changes in owners’ equity reports the changes in owners’ equity for a specific period of time.

(5) Notes to financial statements 财务报表附注

Notes to the accounting statements are further explanations of items presented in the accounting statements, and explanations of items not presented in the accounting statements, etc.

9. Accounting entry 会计分录

Debit: Cash

Credit: Common Stock

10. Basic accounting equation 基本会计等式

Assets = Liabilities + owners’ equity

11. List of present and potential users of financial information 财务信息的使用者

investors, creditors, employees, suppliers, customers, and governmental agencies.

Definitions of Four Categories of Financial Assets

A financial asset or liability held for trading is one that was acquired or incurred principally for the purpose of generating a profit from short-term fluctuations in price or dealers margin. A financial asset should be classified as held for trading if, regardless of why it was acquired, it is part of a portfolio for which there is evidence of a recent actual pattern of short-term profit-taking. Derivative financial assets and derivative financial liabilities are always deemed held for trading unless they are designated and effective hedging instruments.

Held-to-maturity investments are financial assets with fixed or determinable payments and fixed maturity that an enterprise has the positive intent and ability to hold to maturity other than loans and receivables originated by the enterprise.

四类金融资产的定义

为交易而持有的金融资产或金融负债,指主要为了从价格或交易商保证金的短期波动中获利而购置的金融资产或承担的金融负债。一项金融资产不论因何种原因购置,如果它属于

投资组合的组成部分,且有证据说明最近该组合可实际获得短期收益,则该金融资产应归类为为交易而持有的金融资产。对于衍生金融资产和衍生金融负债,除非它们被指定且是有效的套期工具,否则应认为是为交易而持有的金融资产和金融负债.

持有至到期日的投资指具有固定或可确定金额和固定期限,且企业明确打算并能够持有至到期日的金融资产。企业源生的贷款和应收款项不包括在内。

企业源生的贷款和应收款项,指企业直接向债务人提供资金、商品或劳务所形成的金融资产。但打算立即或在短期内就转让的贷款和应收款项不包括在内,而应归类为为交易而持有的金融资产。在本准则中,企业源生的贷款和应收款项不应包括在持有至到期日的投资内,而应另行归类。

可供出售的金融资产,指不属于以下三类的金融资产:(1)企业源生的贷款和应收款项;(2)持有至到期日的投资;(3)为交易而持有的金融资产。

开发阶段

只有当企业可证明以下所有各项时,开发(或内部项目的开发阶段)产生的无形资产应予确认:

1.完成该无形资产,使其能使用或销售,在技术上可行;

2.有意完成该无形资产并使用或销售它;

3.有能力使用或销售该无形资产;

4.该无形资产如何产生很可能的未来经济利益.其中,企业应证明存在着无形资产的产出市场或无形资产本身的市场;如果该无形资产将在内部使用,那么应证明该无形资产的有用性;

5.有足够的技术、财务资源和其他资源支持,以完成该无形资产的开发,并使用或销售该无形资产;

6.对归属于该无形资产开发阶段的支出,能够可靠地计量.

Development Phase

An intangible asset arising from development (or from the development phase of an internal project)should be recognised if, and only if, an enterprise can demonstrate all of the following:

(a)the technical feasibility of completing the intangible asset so that it will be available for use or sale;

(b)its intention to complete the intangible asset and use or sell it;

(c)its ability to use or sell the intangible asset;

(d)how the intangible asset will generate probable future economic benefits. Among other things, the enterprise should demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset;

(e)the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset;

(f)its ability to measure the expenditure attributable to the intangible asset during its development reliably

财务专业术语中英文对照表 英文中文说明 Account Accounting system 会计系统 American Accounting Association 美国会计协会 American Institute of CPAs 美国注册会计师协会 Audit 审计 Balance sheet 资产负债表 Bookkeepking 簿记 Cash flow prospects 现金流量预测 Certificate in Internal Auditing 部审计证书 Certificate in Management Accounting 管理会计证书 Certificate Public Accountant注册会计师 Cost accounting 成本会计 External users 外部使用者 Financial accounting 财务会计 Financial Accounting Standards Board 财务会计准则委员会 Financial forecast 财务预测 Generally accepted accounting principles 公认会计原则 General-purpose information 通用目的信息 Government Accounting Office 政府会计办公室 Income statement 损益表 Institute of Internal Auditors 部审计师协会 Institute of Management Accountants 管理会计师协会 Integrity 整合性 Internal auditing 部审计 Internal control structure 部控制结构 Internal Revenue Service 国收入署 Internal users部使用者 Management accounting 管理会计 Return of investment 投资回报 Return on investment 投资报酬 Securities and Exchange Commission 证券交易委员会

Chemntherapeutic agents 化学疗法 thus xue fiao fa) Chemothcrjipy 化学疔,Z (hija xue Aaa fa) hns the goal of killing or stopping rhe development nf rapidly dividing cells. Examples are Cisplatin, Carboplat in, Bkomycin I 博来霉嗪1 (ftd l3f Sg S-fltinrncjrao 5 氟尿瞪喘(ft/ HiAO m dfinfl), mrthotrExate 甲員媒时{Jia 的 did /ioffk Vincristine fifr chun xJTj/a^, Vinblastine 衣祚碱 (chang chun ;ian}. Taxol and Tawiuvirtn .木戟题(SSfi ben 阳ng 钠* Since the sanK nicchanism (hat kilh malignant cdl or blocks de vela pment of a malignant cell cm have similar effects on a nnrnuil, rap idly dividing celt any of LhcNt agents ciin hax r c btid side clfccts. Some terms of cancer ircitLcd with chemcthera 卩、may cjus,e ihe cancer (o "disappear

常用会计名词(中英文对照)accelerated depreciation method 加速折旧法 account 账户 account payable 应付账款 account receivable 应收账款 accountant会计师、会计人员 accounting会计 accounting cycle 会计循环 accounting equation会计等式 accounting information system 会计信息系统 accrual-basis accounting 应计制会计、权责发生制会计 accrued expense 应计费用、预提费用 accrued revenue应计收入 accumulated depreciation累计折旧 acid-test ratio酸性测试比率,速动比率 additional paid-in capital 超额缴入股本 adjusted trial balance 整后试算平衡表 adjusting entry调整分录 aging-of-accounts method账龄分析法 allowance for doubtful accounts呆帐准备备抵 allowance for uncollectible accounts坏帐准备 allowance method备抵法 amortization 摊销分期偿还 asset资产 audit审计 authorization of stock 额定股本 average-cost method 平均成本法 bad-debt expense 坏帐费用 balance sheet 资产负债表 bank reconciliation 银行存款余额调节表 bank statement 银行对账单 board of directors 董事会 bond 债券 bond discount 债券折价 bond premium 债券溢价

Photoshop字体库中英文对照表 当确实字体时,Photoshop会提示丢失字体,但是提示的字体名称是一串英文字符,即使字体的名称是中文的也是一样。这给我们的带来了困难,很难找到对应的字体来安装。今天要用字体了,所以就收集了下供大家参考希望对大家有帮助! (简体部分) 中文字体名英文字体名文件名PS name汉字数 方正报宋简体FZBaoSong-Z04S FZBSJW FZBSJW—GB1-0 7156 方正粗圆简体FZCuYuan-M03S FZY4JW—GB1-0 7156 方正大标宋简体FZDaBiaoSong-B06SFZDBSJW—GB1-0 7156 方正大黑简体FZDaHei-B02SFZDHTJW—GB1-0 7156 方正仿宋简体FZFangSong-Z02S FZFSJW—GB1-0 7156 方正黑体简体FZHei-B01S FZHTJW—GB1-0 7156 方正琥珀简体FZHuPo-M04S FZHPJW—GB1-0 7156 方正楷体简体FZKai-Z03S FZKTJW—GB1-0 7156 方正隶变简体FZLiBian-S02S FZLBJW—GB1-0 7156 方正隶书简体FZLiShu-S01S FZLSJW—GB1-0 7156 方正美黑简体FZMeiHei-M07S FZMHJW—GB1-0 7156 方正书宋简体FZShuSong-Z01S FZSSJW FZSSJW—GB1-0 7156 方正舒体简体FZShuTi-S05S FZSTJW FZSTJW—GB1-0 7152 方正水柱简体FZShuiZhu-M08S FZSZJW—GB1-0 7156 方正宋黑简体FZSongHei-B07S FZSHJW—GB1-0 7156

语文课程与教学论 名词术语中英文对照表 the Chinese Course and Teaching and Learning Theory in Chinese and English Teaching materials editing teaching materials /Chinese Teaching Materials /edit teaching materials /Uniformed Chinese Teaching Materials /Experimental Teaching Materials /Mother Tongue Teaching Materials /Teaching Materials of the New Course *textbook *reading book *teaching reference book *exercises book *studying plan Technology /Educational Technology /Modern Educational Technology /Educational Technology in Chinese Teaching /multi-media technology /net technology /cloud serving technology *white board *net meeting *chat room *blog Teaching Basic Theory of the Teaching teaching aim teaching task teaching objective teaching model teaching tactics teaching principle teaching program teaching reform teaching case Courseware teaching resources teaching experiment /mother tongue teaching A Term List of 1. 教材( JC ) 教材编写 /语文教材 /编写教材 / 统编教材 /实验教材 /母语教材 /新课程教材 * 课本 * 读本 * 教学参考书(教参) * 练习册 *学案 2. 技术( JS ) / 教育技术 /现代 教育技术 /语文 教育技术 /多媒 体技术 / 网络 技术 /云服务技 术 * 白板 *网 络会议 *聊天室 * 博克 3. 教学 (JX ) 教学基本理论 教学目的 教学 任务 教学目标 教学模式 教学 策略 教学原则 教学大纲 教学 改革 教学案例 教学课件 教学 资源 教学实验 /母语教学

会计术语中英文对照

会计专业术语中英文对照 A (1)ABC 作业基础成本计算 A (2)absorbed overhead 已吸收制造费用 A (3)absorption costing 吸收成本计算 A (4)account 帐户,报表 A (5)accounting postulate 会计假设 A (6)accounting series release 会计公告文件 A (7)accounting valuation 会计计价 A (8)account sale

承销清单 A (9)accountability concept 经营责任概念 A (10)accountancy 会计职业A (11)accountant 会计师A (12)accounting 会计A (13)agency cost 代理成本 A (14)accounting bases 会计基础 A (15)accounting manual 会计手册 A (16)accounting period 会计期间

A (17)accounting policies 会计方针 A (18)accounting rate of return 会计报酬率 A (19)accounting reference date 会计参照日 A (20)accounting reference period 会计参照期间 A (21)accrual concept 应计概念 A (22)accrual expenses 应计费用 A (23)acid test ration 速动比率(酸性测试比率) A (24)acquisition

一、损益表INCOME STATEMENT Aggregate income statement 合并损益表 Operating Results 经营业绩 FINANCIAL HIGHLIGHTS 财务摘要 Gross revenues 总收入/毛收入 Net revenues 销售收入/净收入 Sales 销售额 Turnover 营业额 Cost of revenues 销售成本 Gross profit 毛利润 Gross margin 毛利率 Other income and gain 其他收入及利得 EBITDA 息、税、折旧、摊销前利润(EBITDA) EBITDA margin EBITDA率 EBITA 息、税、摊销前利润 EBIT 息税前利润/营业利润 Operating income(loss)营业利润/(亏损) Operating profit 营业利润 Operating margin 营业利润率 EBIT margin EBIT率(营业利润率) Profit before disposal of investments 出售投资前利润 Operating expenses: 营业费用: Research and development costs (R&D)研发费用 marketing expensesSelling expenses 销售费用 Cost of revenues 营业成本 Selling Cost 销售成本 Sales and marketing expenses Selling and marketing expenses 销售费用、或销售及市场推广费用 Selling and distribution costs 营销费用/行销费用 General and administrative expenses 管理费用/一般及管理费用 Administrative expenses 管理费用 Operating income(loss)营业利润/(亏损) Profit from operating activities 营业利润/经营活动之利润 Finance costs 财务费用/财务成本 Financial result 财务费用 Finance income 财务收益 Change in fair value of derivative liability associated with Series B convertible redeemable preference shares 可转换可赎回优先股B相关衍生负债公允值变动 Loss on the derivative component of convertible bonds 可換股債券衍生工具之損失Equity loss of affiliates 子公司权益损失 Government grant income 政府补助 Other (expense) / income 其他收入/(费用)

设计常用字体库中英文对照表 当确实字体时,Photoshop会提示丢失字体,但是提示的字体名称是 一串英文字符,即使字体的名称是中文的也是一样。这给我们的带来 了困难,很难找到对应的字体来安装。今天要用字体了,所以就收集 了下供大家参考希望对大家有帮助! (简体部分) 中文字体名英文字体名文件名 PS name 汉字数 方正报宋简体 FZBaoSong-Z04S FZBSJW FZBSJW—GB1-0 7156 方正粗圆简体 FZCuYuan-M03S FZY4JW FZY4JW—GB1-0 7156 方正大标宋简体 FZDaBiaoSong-B06S FZDBSJW FZDBSJW—GB1-0 7156 方正大黑简体 FZDaHei-B02S FZDHTJW FZDHTJW—GB1-0 7156 方正仿宋简体 FZFangSong-Z02S FZFSJW FZFSJW—GB1-0 7156 方正黑体简体 FZHei-B01S FZHTJW FZHTJW—GB1-0 7156 方正琥珀简体 FZHuPo-M04S FZHPJW FZHPJW—GB1-0 7156 方正楷体简体 FZKai-Z03S FZKTJW FZKTJW—GB1-0 7156 方正隶变简体 FZLiBian-S02S FZLBJW FZLBJW—GB1-0 7156 方正隶书简体 FZLiShu-S01S FZLSJW FZLSJW—GB1-0 7156 方正美黑简体 FZMeiHei-M07S FZMHJW FZMHJW—GB1-0 7156 方正书宋简体 FZShuSong-Z01S FZSSJW FZSSJW—GB1-0 7156 方正舒体简体 FZShuTi-S05S FZSTJW FZSTJW—GB1-0 7152 方正水柱简体 FZShuiZhu-M08S FZSZJW FZSZJW—GB1-0 7156 方正宋黑简体 FZSongHei-B07S FZSHJW FZSHJW—GB1-0 7156 方正宋三简体 FZSong III-Z05S FZS3JW FZS3JW—GB1-0 7156 方正魏碑简体 FZWeiBei-S03S FZWBJW FZWBJW—GB1-0 7156 方正细等线简体 FZXiDengXian-Z06S FZXDXJW FZXDXJW—GB1-0 7156 方正细黑一简体 FZXiHei I-Z08S FZXH1JW FZXH1JW—GB1-0 7156 方正细圆简体 FZXiYuan-M01S FZY1JW FZY1JW—GB1-0 7156 方正小标宋简体 FZXiaoBiaoSong-B05S FZXBSJW FZXBSJW—GB1-0 7156 方正行楷简体 FZXingKai-S04S FZXKJW FZXKJW—GB1-0 7156

各种专业名称英语词汇中英文对照表

————————————————————————————————作者: ————————————————————————————————日期: ?

各种专业名称英语词汇中英文对照表 哲学Philosophy 马克思主义哲学Philosophy of Marxism 中国哲学ChinesePhilosophy 外国哲学ForeignPhilosophies ?逻辑学Logic?伦理学Ethics 美学Aesthetics 宗教学Science of Religion?科学技术哲学Philosophy of Science andTechnology?经济学Economics?理论经济学Theoretical Economics ?政治经济学PoliticalEconomy ?经济思想史History ofEconomic Thought ?经济史History of Economic 西方经济学WesternEconomics?世界经济World Economics ?人口、资源与环境经济学Population,Resources andEnvironmentalEconomics 应用经济学Applied Economics 国民经济学National Economics?区域经济学Regional Economics ?财政学(含税收学)Public Finance (includingTaxation) 金融学(含保险学) Finance (including Insurance)?产业经济学Industrial Economics ?国际贸易学International Trade 劳动经济学Labor Economics ?统计学Statistics ?数量经济学Quantita tive Economics ?中文学科、专业名称英文学科、专业名称 国防经济学National Defense Economics?法学Law 法学Science of Law ?法学理论Jurisprudence?法律史Legal History ?宪法学与行政法学Constitutional Law and Administrative Law 刑法学Criminal Jurisprudence 民商法学(含劳动法学、社会保障法学)Civil Law and Commercial Law (i ncluding Science of LabourLawand Science ofSocial Sec urityLaw)?诉讼法学Science of ProcedureLaws ?经济法学Sc ience ofEconomic Law ?环境与资源保护法学Science ofEnvironment andNatural Resources Protection Law 国际法学(含国际公法学、国际私法学、国际经济法学、)Internationallaw (including International Public law, International PrivateLaw a

会计名词中英文对照 abnormal damage and loss 非常损失abnormality 异常性 absorption costing 归纳成本法 accelerated depreciation method 加速折旧法 accelerated deprecviation 加速折旧 account 会计科目 account analysis method账户分析法 Accountant会计人员A accounting basis 会计基础 accounting changes会计变动 accounting cycle会计循环 accounting error 会计错误 accounting income会计所得 Accounting Report 会计报告AR accounts receivable 应收帐款 accountting rate of return 会计报酬率 accrual basis 应计基础 accrued expenses 应计费用 accrued items 应计项目 accrued liabilities应计负债

accrued revenues 应计收益 accumulated depreciation 累计折旧accumulated rights累积权益 acid-test ratio(quick ratio)酸性测验比率 activity accounting 作业会计( 责任会计) activity based cost system 作业制成本制度 activity or productivity analysis 活动/生产能力activity variance 作业差异 activity-based accounting 作业制会计 activity-based costing 作业制成本 actual costing 实际成本法 actual costs 实际成本 additional markup再加价 additional markup cancellation 再加价取销adjusting 调整 aging of accounts receivable 帐龄分析法 all financial resources concept 全部财务资源观念allowable cost 可允成本 allowance for doubtful accounts 备抵坏帐allowance method 备抵评价法 American Accounting Association 美国会计学会AAA annuity 年金 applied factory overhead已分摊制造费用appraisal 估价 appraisal costs 鉴定成本

汉字英文对照 方正报宋简体FZBaoSong-Z04S FZBSJW FZBSJW—GB1-0 7156方正粗圆简体FZCuYuan-M03S FZY4JW FZY4JW—GB1-07156 方正大标宋简体FZDaBiaoSong-B06S FZDBSJW FZDBSJW—GB1-07156 方正大黑简体FZDaHei-B02S FZDHTJW FZDHTJW—GB1-0 7156 方正仿宋简体FZFangSong-Z02S FZFSJW FZFSJW—GB1-07156 方正黑体简体FZHei-B01S FZHTJW FZHTJW—GB1-07156 方正琥珀简体FZHuPo-M04S FZHPJW FZHPJW—GB1-07156 方正楷体简体FZKai-Z03S FZKTJW FZKTJW—GB1-0 7156 方正隶变简体FZLiBian-S02S FZLBJW FZLBJW—GB1-07156 方正隶书简体FZLiShu-S01S FZLSJW FZLSJW—GB1-07156 方正美黑简体FZMeiHei-M07S FZMHJW FZMHJW—GB1-07156 方正书宋简体FZShuSong-Z01S FZSSJW FZSSJW—GB1-07156 方正舒体简体FZShuTi-S05S FZSTJW FZSTJW—GB1-0 7152 方正水柱简体FZShuiZhu-M08S FZSZJW FZSZJW—GB1-07156 方正宋黑简体FZSongHei-B07S FZSHJW FZSHJW—GB1-07156 方正宋三简体FZSong III-Z05S FZS3JW FZS3JW—GB1-07156 方正魏碑简体FZWeiBei-S03S FZWBJW FZWBJW—GB1-0 7156 方正细等线简体FZXiDengXian-Z06S FZXDXJW FZXDXJW—GB1-0 7156 方正细黑一简体FZXiHei I-Z08S FZXH1JW FZXH1JW—GB1-07156 方正细圆简体FZXiYuan-M01S FZY1JW FZY1JW—GB1-07156

财务术语中英文对照大全一、会计与会计理论 会计 accounting 决策人 Decision Maker 投资人 Investor 股东 Shareholder 债权人 Creditor 财务会计 Financial Accounting 管理会计 Management Accounting 成本会计 Cost Accounting 私业会计 Private Accounting 公众会计 Public Accounting 注册会计师 CPA Certified Public Accountant 国际会计准则委员会 IASC 美国注册会计师协会 AICPA 财务会计准则委员会 FASB 管理会计协会 IMA 美国会计学会 AAA 税务稽核署 IRS 独资企业 Proprietorship 合伙人企业 Partnership 公司 Corporation 会计目标 Accounting Objectives 会计假设 Accounting Assumptions 会计要素 Accounting Elements 会计原则 Accounting Principles 会计实务过程 Accounting Procedures 财务报表 Financial Statements 财务分析Financial Analysis 会计主体假设 Separate-entity Assumption 货币计量假设 Unit-of-measure Assumption 持续经营假设 Continuity(Going-concern) Assumption 会计分期假设 Time-period Assumption 资产 Asset 负债 Liability 业主权益 Owner's Equity 收入 Revenue 费用 Expense

初级会计 初级会计 会计术语名称英文名称 对账(checking) 对应账户(corresponding accounts) 定期清查(Periodic checking method) 定期盘存制(periodic inventory system) 订本式账簿(bound book) 调整账户(adjustment accounts) 调整分录(adjusting journal entry) 单式记账凭证(single account title voucher) 单式记账法(single-entry bookkeeping) 从属账户(Secondary accounts) 成本计算账户(costing accounts) 财产清查(physical inventory) 簿记(bookkeeping) 不定期清查(non-periodic checking method) 补充登记法(correction by extre recording) 表外账户(off-balance sheet accounts) 备抵账户(provision accounts) 备抵附加账户(provision and adjunct accounts) 备查账簿(memorandvn) 序时账簿(book of chronological entry) 一次凭证(single-record document)银行存款日记账(deposit journal) 永续盘存制(perpetual inventory system) 原始凭证(source document) 暂记账户(suspense accounts) 增减记账法(increase-decrease bookkeeping) 债权结算账户(accounts for settlement of claim)债权债务结算账户(accounts for settlement of claim and debt)债务结算账户(accounts for settlement of debt) 账户(account) 账户编号(Account number) 账户对应关系(debit-credit relationship) 账项调整(adjustment of account)

术语表 Acceptance Criteria–接受标准:接受测试结果的数字限度、范围或其他合适的量度标准。Active Pharmaceutical Ingredient(API)(or Drug Substance)-活性要用成分(原料药)旨在用于药品制造中的任何一种物质或物质的混合物,而且在用于制药时,成为药品的一种活性成分。此种物质在疾病的诊断,治疗,症状缓解,处理或疾病的预防中有药理活性或其他直接作用,或者能影响机体的功能和结构。 API Starting Material–原料药的起始物料:用在原料药生产中的,以主要结构单元被并入该原料药的原料、中间体或原料药。原料药的起始物料可能是在市场上有售,能够根据合同或商业协议从一个或多个供应商处购得,或者自己生产。原料药的起始物料通常有特定的化学特性和结构。 Batch(or Lot)-批:有一个或一系列工艺过程生产的一定数量的物料,因此在规定的限度内是均一的。在连续生产中,一批可能对应与生产的某以特定部分。其批量可规定为一个固定数量,或在固定时间间隔内生产的数量。 Batch Number(or Lot Number)-批号用于标识一批的一个数字、字母和/或符号的唯一组合,从中可确定生产和销售的历史。 Bioburden–生物负载:可能存在与原料、原料药的起始物料、中间体或原料药中的微生物的水平和种类(例如,治病的或不治病的)。生物负载不应当当作污染,除非含量超标,或者测得治病生物。 Calibration–校验:证明某个仪器或装置在一适当的量程范围内测得的结果与一参照物,或可追溯的标准相比在规定限度内。 Computer System–计算机系统:设计安装用于执行某一项或一组功能的一组硬件元件和关联的软件。 Computerized System–计算机化系统与计算机系统整合的一个工艺或操作。Contamination–污染:在生产、取样、包装或重新包装、贮存或运输过程中,具化学或微生物性质的杂质或外来物质进入或沾染原料、中间体或原料药。 Contract Manufacturer–协议制造商:代表原制造商进行部分制造的制造商。 Critical–决定性的:用来描述为了确保原料药符合规格标准,必须控制在预定范围内的工艺步骤、工艺条件、测试要求或其他有关参数或项目。 Cross-Contamination–交叉污染:一种物料或产品对另一种物料或产品的污染。 Deviation–偏差:对批准的指令或规定的标准的偏离。 Drug(Medicinal)Product–药品:经最后包装准备销售的制剂(参见Q1A) Drug Substance–药物见原料药 Expiry Date(or Expiration Date)-有效期:原料药容器/标签上注明的日期,在此规定时间内,该原料药在规定条件下贮存时,仍符合规格标准,超过这以期限则不应当使用。 Impurity–杂质:存在与中间体或原料药中,任何不希望得到的成分。 Impurity Profile–杂质概况:对存在于一种原料药中的已知和未知杂质的描述。 In-Process Control(or Process Control)-中间控制:生产过程中为监测,在必要时调节工艺和/或保证中间体或原料药符合其规格而进行的检查。 Intermediate–中间体:原料药工艺步骤中生产的、必须经过进一步分子变化或精制才能成为原料药的一种物料。中间体可以分离或不分离。 Manufacture–制造:物料的接收、原料药的生产、包装、重新包装、贴签、重新贴签、质量控制、放行、贮存和分发以及相关控制的所有操作。 Material–物料:原料(起始物料,试剂,溶剂),工艺辅助用品,中间体,原料药和包装及贴签材料的统称。

高分子专业术语中英文对照表

加工processing 反应性加工reactive processing 等离子体加工plasma processing 加工性processability 熔体流动指数melt [flow] index 门尼粘度Mooney index 塑化plasticizing 增塑作用plasticization 内增塑作用internal plasticization 外增塑作用external plasticization 增塑溶胶plastisol 增强reinforcing 增容作用compatibilization 相容性compatibility 相溶性intermiscibility 生物相容性biocompatibility 血液相容性blood compatibility 组织相容性tissue compatibility 混炼milling, mixing 素炼mastication 塑炼plastication 过炼dead milled 橡胶配合rubber compounding 共混blend 捏和kneading 冷轧cold rolling 压延性calenderability 压延calendering 埋置embedding 压片preforming 模塑molding 模压成型compression molding 压缩成型compression forming 冲压模塑impact moulding, shock moulding 叠模压塑stack moulding 复合成型composite molding 注射成型injection molding 注塑压缩成型injection compression molding 射流注塑jet molding 无流道冷料注塑runnerless injection molding 共注塑coinjection molding 气辅注塑gas aided injection molding 注塑焊接injection welding 传递成型transfer molding

会计科目中英文对照表 二、负债类Liability 短期负债Current liability 2101 短期借款Short-term borrowing 2111 应付票据Notes payable 银行承兑汇票Bank acceptance 商业承兑汇票Trade acceptance 2121 应付账款Account payable 2131 预收账款Deposit received 2141 代销商品款Proxy sale goods revenue 2151 应付工资Accrued wages 2153 应付福利费Accrued welfarism 2161 应付股利Dividends payable 2171 应交税金T ax payable '217101 应交增值税value added tax payable '21710101 进项税额Withholdings on VAT '21710102 已交税金Paying tax '21710103 转出未交增值税Unpaid VAT changeover '21710104 减免税款T ax deduction '21710105 销项税额Substituted money on VAT '21710106 出口退税T ax reimbursement for export '21710107 进项税额转出Changeover withnoldings on VAT '21710108 出口抵减内销产品应纳税额Export deduct domestic sales goods tax '21710109 转出多交增值税Overpaid VAT changeover '21710110 未交增值税Unpaid VAT '217102 应交营业税Business tax payable '217103 应交消费税Consumption tax payable '217104 应交资源税Resources tax payable '217105 应交所得税Income tax payable '217106 应交土地增值税Increment tax on land value payable '217107 应交城市维护建设税Tax for maintaining and building cities payable '217108 应交房产税Housing property tax payable '217109 应交土地使用税Tenure tax payable '217110 应交车船使用税Vehicle and vessel usage license plate tax(VVULPT) payable '217111 应交个人所得税Personal income tax payable 2176 其他应交款Other fund in conformity with paying 2181 其他应付款Other payables 2191 预提费用Drawing expense in advance 其他负债Other liabilities 2201 待转资产价值Pending changerover assets value 2211 预计负债Anticipation liabilities

Photoshop字体库中英文对照表 当确实字体时,Photoshop会提示丢失字体,但是提示的字体名称是一串英文字符,即使字体的名称是中文的也是一样。这给我们的带来了困难,很难找到对应的字体来安装。今天要用字体了,所以就收集了下 供大家参考 希望对大家有帮助! (简体部分) 中文字体名 英文字体名 文件名 PS name 汉字数 方正报宋简体 FZBaoSong‐Z04S FZBSJW FZBSJW—GB1‐0 7156 方正粗圆简体 FZCuYuan‐M03S FZY4JW FZY4JW—GB1‐0 7156 方正大标宋简体 FZDaBiaoSong‐B06S FZDBSJW FZDBSJW—GB1‐0 7156 方正大黑简体 FZDaHei‐B02S FZDHTJW FZDHTJW—GB1‐0 7156 方正仿宋简体 FZFangSong‐Z02S FZFSJW FZFSJW—GB1‐0 7156 方正黑体简体 FZHei‐B01S FZHTJW FZHTJW—GB1‐0 7156 方正琥珀简体 FZHuPo‐M04S FZHPJW FZHPJW—GB1‐0 7156 方正楷体简体 FZKai‐Z03S FZKTJW FZKTJW—GB1‐0 7156 方正隶变简体 FZLiBian‐S02S FZLBJW FZLBJW—GB1‐0 7156 方正隶书简体 FZLiShu‐S01S FZLSJW FZLSJW—GB1‐0 7156 方正美黑简体 FZMeiHei‐M07S FZMHJW FZMHJW—GB1‐0 7156 方正书宋简体 FZShuSong‐Z01S FZSSJW FZSSJW—GB1‐0 7156 方正舒体简体 FZShuTi‐S05S FZSTJW FZSTJW—GB1‐0 7152 方正水柱简体 FZShuiZhu‐M08S FZSZJW FZSZJW—GB1‐0 7156 方正宋黑简体 FZSongHei‐B07S FZSHJW FZSHJW—GB1‐0 7156 方正宋三简体 FZSong III‐Z05S FZS3JW FZS3JW—GB1‐0 7156 方正魏碑简体 FZWeiBei‐S03S FZWBJW FZWBJW—GB1‐0 7156 方正细等线简体 FZXiDengXian‐Z06S FZXDXJW FZXDXJW—GB1‐0 7156 方正细黑一简体 FZXiHei I‐Z08S FZXH1JW FZXH1JW—GB1‐0 7156 方正细圆简体 FZXiYuan‐M01S FZY1JW FZY1JW—GB1‐0 7156 方正小标宋简体 FZXiaoBiaoSong‐B05S FZXBSJW FZXBSJW—GB1‐0 7156 方正行楷简体 FZXingKai‐S04S FZXKJW FZXKJW—GB1‐0 7156 方正姚体简体 FZYaoTi‐M06S FZYTJW FZYTJW—GB1‐0 7156 方正中等线简体 FZZhongDengXian‐Z07S FZZDXJW FZZDXJW—GB1‐0 7156 方正准圆简体 FZZhunYuan‐M02S FZY3JW FZY3JW—GB1‐0 7156 方正综艺简体 FZZongYi‐M05S FZZYJW FZZYJW—GB1‐0 7156 方正彩云简体 FZCaiYun‐M09S FZCYJW FZCYJW—GB1‐0 7156 方正隶二简体 FZLiShu II‐S06S FZL2JW FZL2JW—GB1‐0 7156 方正康体简体 FZKangTi‐S07S FZKANGJW FZKANGJW—GB1‐0 7156 方正超粗黑简体 FZChaoCuHei‐M10S FZCCHJW FZCCHJW—GB1‐0 7156 方正新报宋简体 FZNew BaoSong‐Z12S FZNBSJW FZNBSJW—GB109 7156 方正新舒体简体 FZNew ShuTi‐S08S FZNSTJW FZNSTJW—GB1‐0 7156 方正黄草简体 FZHuangCao‐S09S FZHCJW FZHCJW—GB1‐0 6763 方正少儿简体 FZShaoEr‐M11S FZSEJW FZSEJW—GB1‐0 7156 方正稚艺简体 FZZhiYi‐M12S FZZHYJW FZZHYJW—GB1‐0 7156 方正细珊瑚简体 FZXiShanHu‐M13S FZXSHJW FZXSHJW—GB1‐0 7156 方正粗宋简体 FZCuSong‐B09S FZCSJW FZCSJW—GB1‐0 7156